Debunking the Myth of Disruptive Innovation: How Disruptions Work in the AI age

Today, many disruptors upend industries without passing through the so-called “disruptive innovation” stage (Christensen, 1997). For example, Uber is one of the classic cases that do not fit into what Christensen originally called disruptors concerning disruptive innovation. In The Innovator’s Dilemma, what he characterized as disruptive innovation is the one that originates from the lower end of the market and progressively moves to the mainstream. The question to consider is: Is the theory itself being upended? Or at least, did the theory explain only one form of disruption among others? Maybe. Uber’s platform is a classic case that exemplifies this. It did not start at the so-called low end and did not convert those who did not utilize taxis into new buyers (Christensen et al., 2015).

So, Uber cannot be categorized as a true disruptor in the true sense of disruptive innovation. Accordingly, if Uber’s innovation cannot be called disruptive as Christensen posits, given that it did not spring from where the theory predicts or assumes to come from, it seems to be a disruptive innovation 2.0—or simply disruption 2.0—assuming that Christensen’s theory is disruptive innovation 1.0, or disruption 1.0. Why are people confusing disruptive innovation with what it is not? At least in Christensen’s view, the problem is that the concept’s popularity may have confused its original definition (Christensen et al., 2015).

However, while this may be true, Christensen’s theory has recently come under the microscope for scrutiny, first from his fellow Professor Jill Lepore (2014) at Harvard. As a historian, she asked for more predictive proof of his theory, wanting clear evidence of the theory’s validity test, an essential marker in scientific research. She questioned the accuracy of Christensen’s approach to data gathering and interpretation of historical corroboration—even suggesting that his sources were dubious and his logic questionable.

Another extensive study by leading scholars, including Andrew A. King of the Tuck School of Business (King & Baatartogtokh, 2015), tried to ascertain the conformity of the touted theory to the cases. Their findings suggest that less than 10% of the cases displayed the four essential characteristics of Christensen’s disruptive innovation theory, indicating a big hole in the theory. However, to his credit, Christensen is a first-rate scholar whose contribution to the field can’t be ignored or easily discounted. To whom we may be all indebted, given the deep insights gleaned from his theory.

We can all agree that when there is a huge gap between a theory and the inner workings of the real world, the theory needs a review or at least an adjustment. Things change quickly in today’s complex and high-tech environment; what is valid today could swiftly become a leading theory’s flaws tomorrow or even make the theory questionable. So, the way forward is that theories, like firms, need to become more agile to stay relevant.

To be sure, the Christensen proposition of disruption is market-based. We believe that firms need to broaden their view concerning disruption including nonmarket disruptions. Indeed, according to our experience, most businesses and industries are caught somewhere between the two forms—market and nonmarket disruptions. Moreover, beyond the hyped market-fueled disruption regarding technologies, business models, and product innovation, disruptions in our view seem to be moving in waves that need to be thoroughly considered by executives so they may be able to prioritize their strategic responses regarding resource allocation and choices among others as well as to enhance their likelihood of success.

In other words, several decades ago, nonmarket disruptions and strategies were neglected across corporate boardrooms, given that during those decades, the link and impact of these types of disruptions on firms and industries appear to have been less understood. As a result, nonmarket strategies were given lip service. The second wave began around 40 years ago and was characterized by great academic research on nonmarket strategies (Mellahi et al., 2015) with mild technology-induced disruptions. Today, the third wave is characterized by huge nonmarket disruptions compounded by sprawling, fast-paced, technology-enabled disruptions.

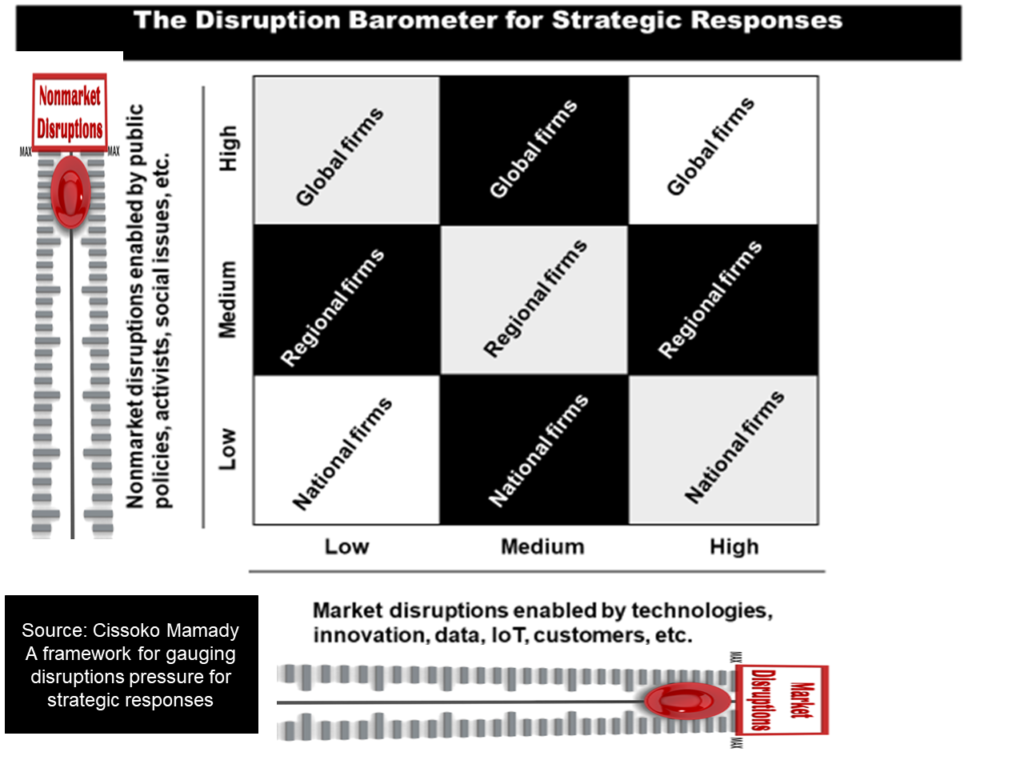

So, most organizations and industries today are caught between these nonexclusive yet unpredictable types of disruptions. On the one hand, companies need to be ahead of the curve of market-based disruptions through product or business model innovations; for example, at the same time, they need to be proactive in dealing with nonmarket-induced disruptions regarding social issues for example. Moreover, we have categorized the nonmarket-originated disruptions into three broad categories—national, regional, and global. In our experience, we believe most businesses fall into one of these categories regarding nonmarket-powered disruptions.

In other words, regarding market-fueled disruptions, most corporations or industries today are increasingly being upended by medium to high disruptions. However, regarding nonmarket-fueled disruptions, depending on the firm’s size and its footprint across the globe—physical, digital, transactional, etc.—it can be upended by national, regional, or global nonmarket-induced disruptions. Therefore, to have a winning strategy, it needs to craft its nonmarket strategic responses accordingly while aligning these responses to its market strategy—the one familiar to most of us.

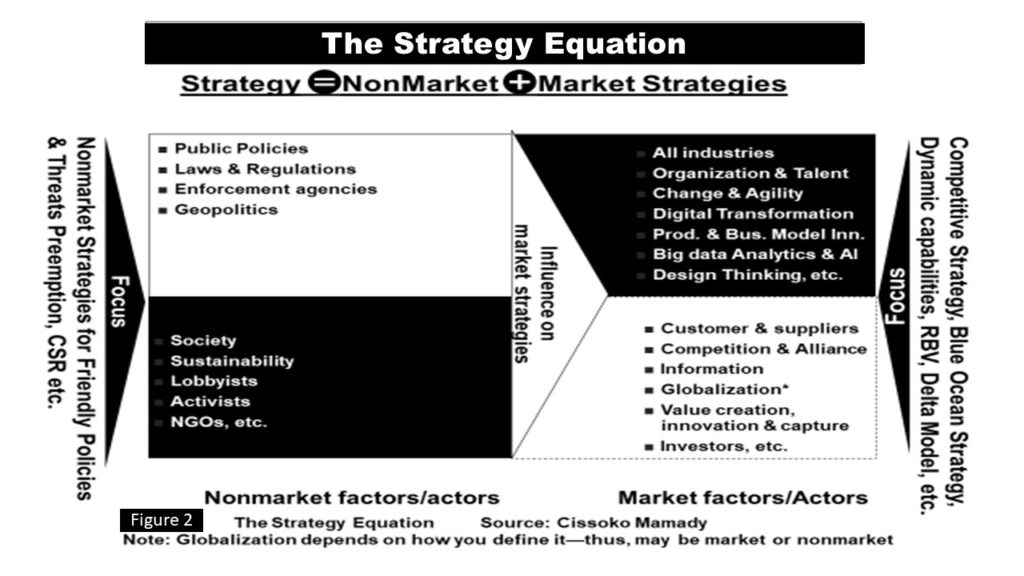

Indeed, we dubbed the sum of these two interrelated components of strategy as “The Strategy Equation.” In other words, strategy, particularly the winning one (fit for the digital age) equals market plus nonmarket strategies. To be sure, these two components of a firm’s strategy need to be crafted with an eye on the congruence aspect to respond effectively to the two forms of disruptions. For example, consider Facebook; during the first years of its existence, it was more focused on responding to market-caused disruptions (products and business model innovations) with respect to other competing platforms wanting to eat its lunch, such as Myspace, Friendster, Twitter and others—according to the platform’s co-founder (Hughes, 2019).

However, in the past two years, since January 2017, given the mounting pressures across the globe regarding fake news within its platform ecosystems, election interference from dangerous foreign actors, privacy issues, and the like, the firm has doubled down on its nonmarket strategies lately, which was previously on the back seat (Buckley, 2018; Pegg, 2019; Bernal, 2019). So, it has upgraded its nonmarket firepower by hiring a special-interest-focused executive—the former British deputy prime minister, Nick Clegg, with a reported compensation of nearly $3.8 million—to deal with the political, legal, and regulatory matters across the globe, particularly on the old continent (MacShane, 2018). As of this writing, Facebook is competing at the two extremes of disruption—extraordinary market-powered disruptions compounded by intense nonmarket-induced disruptions regarding the uncertain political environment and high social pressures. To be sure, Facebook is not alone around the high disruption corners of the barometer; several other leading tech firms are also competing at the two extremes of the disruption barometer, given the global nature of their business concerning Internet customer data, privacy, and transactions. This is one of the reasons most of these companies are highly involved in nonmarket strategies regarding political engagements.

Similarly, Europe-centric nonmarket disruption pressures, such as Brexit, Open Banking, and PSD2, which we called regional nonmarket disruptions on our disruption barometer, significantly affect firms, such as banks and automakers, among others operating in that region. For this reason, the leading British carmaker, Jaguar Land Rover, plans to dismiss over 10% of its workforce (Knowledge@Wharton, 2019). Yet, these nonmarket-fueled disruptions regarding PSD2 have compounded the familiar market-fueled disruptions by inviting other challengers, such as Fintechs or competitors from adjacent industries to the banking sector. As a result, businesses operating in Europe will have to respond strategically to huge nonmarket disruptions derived from politics and public policies and still respond to the medium-to-high market disruption of their supply chain, investments, and APIs.

Similarly, Europe-centric nonmarket disruption pressures, such as Brexit, Open Banking, and PSD2, which we called regional nonmarket disruptions on our disruption barometer, significantly affect firms, such as banks and automakers, among others operating in that region. For this reason, the leading British carmaker, Jaguar Land Rover, plans to dismiss over 10% of its workforce (Knowledge@Wharton, 2019). Yet, these nonmarket-fueled disruptions regarding PSD2 have compounded the familiar market-fueled disruptions by inviting other challengers, such as Fintechs or competitors from adjacent industries to the banking sector. As a result, businesses operating in Europe will have to respond strategically to huge nonmarket disruptions derived from politics and public policies and still respond to the medium-to-high market disruption of their supply chain, investments, and APIs.

In short, the aforementioned nonmarket disruptions are Europe-centric, while their induced market-fueled disruptions can be just European or global in magnitude. So, focusing on the well-hyped market-related disruptions, such as disruptive innovation, which we termed disruption 1.0, or disruption à la Uber, which we dubbed disruption 2.0 while ignoring the nonmarket ones, will spell disaster. Our strategy framework above, called “The Strategy Equation,” will serve as a guide for disrupting or responding to disruption in the digital age given that the 21th-century disruptions are different from those at the end of the 20th century, which Clayton Christensen vividly depicted in his theory of disruptive innovation.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.