M-Pesa and FinTech Around the World: How the Banking Sector got Disrupted?

An old saying about entrepreneurship suggests that business is all about problem-solving. When it comes to disruptive entrepreneurship, it is to identify and address unmet needs with an innovative business model to provide better solutions than ever before. Here is that classic business problem that cries out for solutions:

As of 2014, we had almost 1.95 billion people on the planet with neither traditional nor mobile banking accounts, often called the unbanked or underbanked, nearly 35% of the grown-ups worldwide. In other words, approximately one-third of the global adult population is in desperate need of financial inclusion yet ignored by the traditional banking system, revealed Demigruc-Kunt et al., in 2015. In addition, regarding economic development, the value of mobile phones has been well documented. In fact, each additional cellular phone per 10 individuals in less developed countries results in more than 0.55% points boost to their gross domestic product, that is, their GDP.

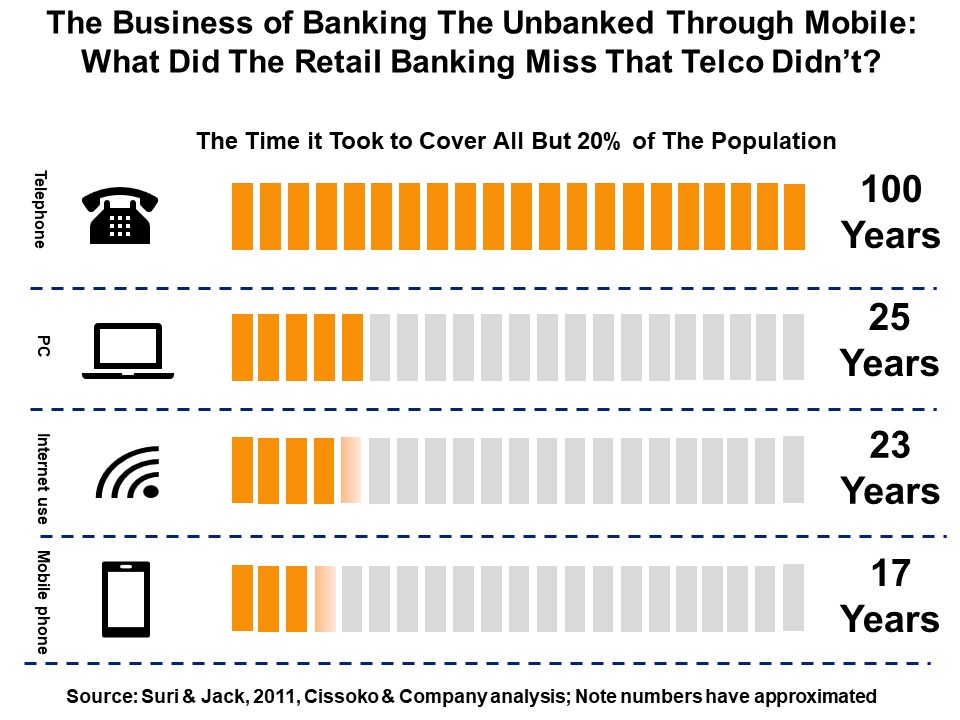

With all these facts and compelling moral reasons regarding financial inclusion, the legacy banking system has been slow to provide basic banking services to this segment of the population for decades. Thanks to the dramatic reduction of the telecommunication infrastructure costs ushered in by the rapid advances in digital technologies, the banking sector became ripe for disruption. As far as technology adoption is concerned, the mobile was arguably one of the fastest. The telephone took almost a century to cover all but 20% of the population. In the case of PCs and the Internet, it took nearly a quarter-century to cover all but 20% of the population. But to gain the same adoption regarding coverage, it took almost 17 years for cell phones, according to Suri and Jack 2011 findings.

Indeed, the Philippines—not Silicon Valley—is the birthplace of Fintech as we know it. Launched in December 2000, SMART Money of SMART Communications Inc., a wireless telecom firm in partnership with first eBank, was the only mobile payment service operating in the world. The world is littered with hundreds across developed and developing economies. This boom in availability has been compounded by the number of people today who have mobile phones.

Again, the rapid digitalization of the business landscape, compounded by the rise of the cellphone-addicted millennials and Generation Z, has exposed the glaring flaws in our financial system, particularly the retail banking services. On top of this, in recent years, the legacy ecosystem and compliance-heavy model of the traditional banking system have been upended by open banking in the United Kingdom and the Second Payment Services Directive (PSD2) in Europe. The mobile phenomenon’s unbundling of the banking ecosystem, which was first seen as just a distraction or a fad, has become the banking industry’s panic moment compounded by other disruptions from other Fintech startups taking advantage of the Internet by using their technological prowess.

The first known mobile banking startup on the African continent is Wizzit, which began its business operations in 2004 and now has more than five dozen employees on its payroll as of 2019 (Wizzit, 2019). Arguably beyond Africa, this Fintech is one of the pioneers of mobile banking in the developing world. Like many of its competitors in the Fintech arena, the firm operated without any formal physical presence—at least in the beginning. Instead, it teamed up with a network of firms, including financial institutions with a physical presence that enabled its customers to do the basic retail banking such as depositing and withdrawing cash through some partnership, given that, unlike Tanzania, regulators in South Africa treat mobile banking like any other legacy banks, was reported by Robb in 2015

The explosion of smartphones across the developing world has meant that one of the best options to get these unbanked and underbanked populations into the financial system is mobile banking. So, in the early days of its introduction in 2004, the noble goal of Wizzit was to provide the unbanked people in its native South Africa access to badly needed banking services through their mobile devices, given that millions of people lacked (and still lack) these basic services across the country.

A few years later (in 2007 to be precise), the relentless attacks and pressures mounted again on the retail banking sector when M-Pesa began operations in Kenya through its corporate parent Vodafone’s subsidiary Safaricom, which was launched in 1997. These new developments in mobile banking became possible thanks to the British grant to Vodafone through its development body (DFID), which enables the concept of transferring money through the mobile phone as we know it today, noted De Vos in 2014 and again by Suri and his colleague Jack in 2011,

Within this small economy of $75 billion (Trading Economics, 2019)—thousands of miles away from the Western-dominant financial hub—M-Pesa enrolled nearly 1,000,000 users within 12 months of its rollout (Dahir, 2018). The world of finance, particularly the banking and telecom sectors, received a strong message: the time of complacency-induced blindness was over.

Then, in 2010, bKash, another trailblazer, was launched in Bangladesh as a BRAC-controlled mobile banking startup (bKash, 2019). After 29 months of its launch, the platform registered more than 10 million users as reported by Chen in 2014. Its growth was so spectacular within a country well-known for its tradition of microfinance—Fortune magazine listed the Fintech among the top influential businesses that changed the world in 2017—given that more than 20% of Bangladeshi grown-ups now use bKash with a little shy of 5 million transactions occurring per day, revealed Dhaka Tribune in 2017. Through the ensuing competition, these entries by startups put pressure on the fees of banks and remittance services such as MoneyGram and Travelex across emerging markets. The trends continue to grow; the volume of mobile-powered products grew by 550% in the six years through 2012, according to Brookings Institution data, noted Handjiski at Brookings in 2015.

However, unlike the business model of M-Pesa in Kenya and bKash in Bangladesh, Wizzit’s business model in the early days was based on the assumption that the people unbanked or underbanked have the same needs and wants as those in the West or at least the affluent segment of South African society. According to our experience, the unbanked people at the base of the development pyramid did not need all the features of retail banking accounts like those living in advanced countries.

Instead, they just need the basic service —sending and receiving money from parents, friends, and other family members via mobile banking—given that most are struggling within their respective economy’s informal sector. One of the reasons why the people living in these impoverished countries want just the basics of retail banking mentioned above—seems to be the glaring distrust of the government, the financial establishments, and the like regarding their reliability – according to Tarun Khanna of Harvard (Knowledge@Wharton, 2019) compounded by high financial illiteracy. In other words, many doubt their government’s capabilities to ensure their savings when banks get into financial trouble.

The key questions are: What it takes to win, and what are the characteristics of the countries where mobile banking has been successful? First, winning entails a granular understanding of the need-related challenges that this huge market faces and building a business model that addresses these needs head-on.

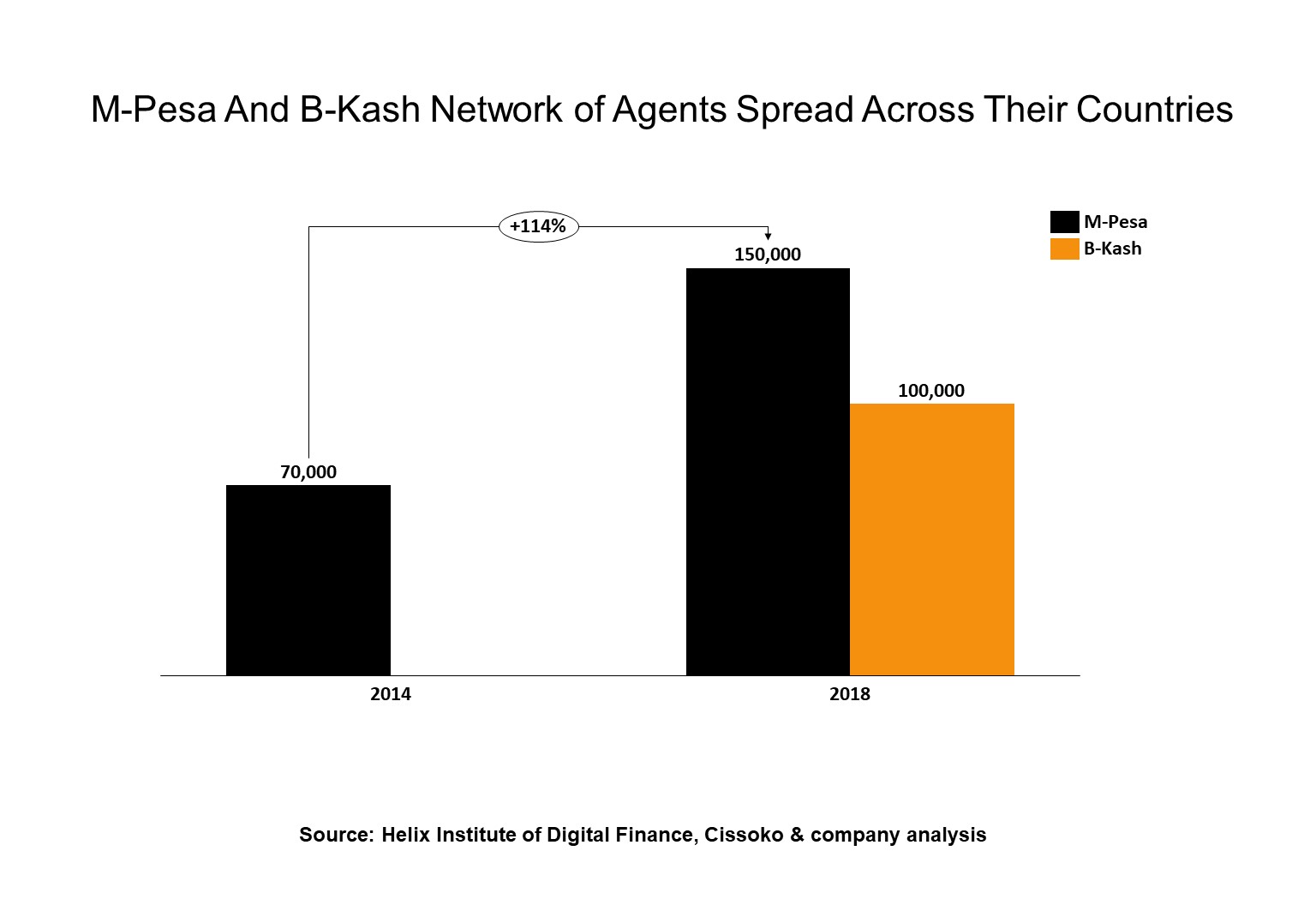

Second, it requires developing a winning agent web through large diffusion regarding geographic distribution, size, etc. (Helix Institute of Digital Finance, 2017). Also, the qualitative aspect of managing the web of agents and building a strategic relationship with them is crucial for winning (Du, 2019). For example, one of the key success factors of M-Pesa in Kenya hinges on its business model based on an ever-growing network of agents, which has been growing by an average of 83 agents per day within the three years through 2014 to more than 70, 000 agents littered across the country (Van Der Berg, 2014). Four years later, in 2018, the world’s most successful mobile banking platform doubled its number of agents across its network to surpass 150,000 (Dahir, 2018a). Similarly, bKash followed in the footsteps of M-Pesa regarding the agents’ web. As of this writing, the disruptor has over 100,000 agents littered across Bangladesh, according to the Helix Institute of Digital Finance in 2017.

However, several observers have cited the critical lack of this network of agents across South Africa as one of the causes of M-Pesa’s epic failure in its foray into South Africa in 2010. But after learning from its mistakes, the disruptor was back again in South Africa in 2014 with an adequate agent network like Kenya.

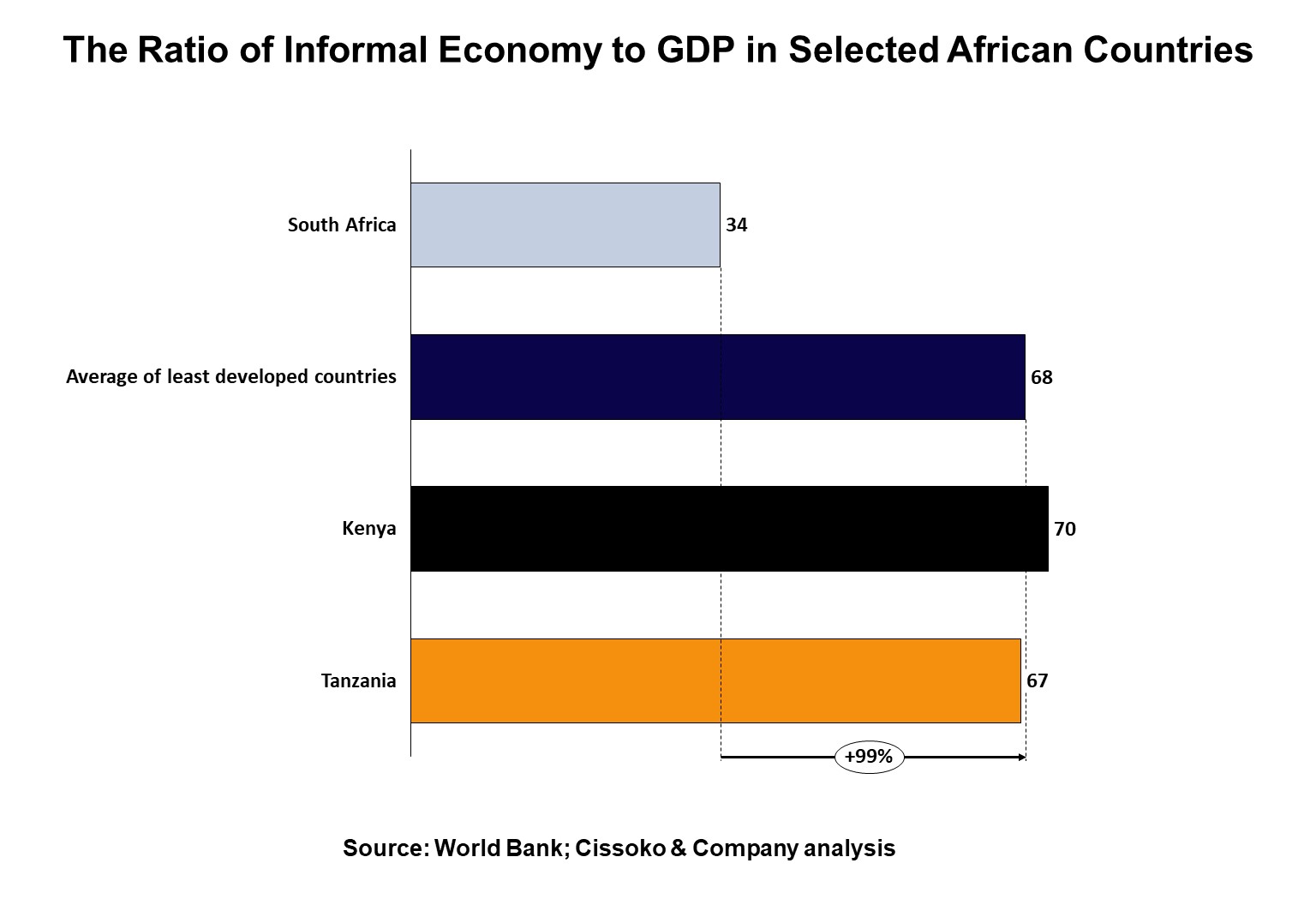

Third, we believe that the proportion of the informal economy to the formal economy on top of a Fintech-friendly regulatory environment combined with a winning business model can shade some light, given that most of the countries in which mobile banking has been successful have a good regulatory environment with a higher ratio of the informal economy to the gross domestic product (DGP). In most cases, according to the World Bank’s data, this ratio is around or higher than the World Bank’s global average of the informal economy to GDP for the least developed countries, which is 67.5% of the GDP. For example, unlike South Africa (34% of the informal economy to GDP), which presents formidable challenges to crack for a mobile banking Fintech—Kenya has an informal economy to GDP of around 70%—in Tanzania, another country where M-Pesa gained ground, the ratio is 67%.

Similarly, in Bangladesh, the home of bKash—one of the world’s most successful mobile banking startups—this ratio is 64% of the GDP. As a result of this macro factor, arguably, M-Pesa and bKash grew quickly after launching their platforms in their respective countries on top of a Fintech-friendly regulatory environment and other aforementioned factors. As far as mobile banking is concerned, M-Pesa and bKash are some of the most well-known success stories. M-Pesa’s platform is so successful that Kenya regulators were reportedly worried about the potential of the platform disrupting the economy. By 2015, more than 20 million Kenyans were using M-Pesa, through which they transacted almost $30 billion. That is, nearly half of the country’s gross domestic product (GDP) at the time.

bKash’s success created an inward gravitational pool of investments from famous development champions, such as the International Finance Corporation (IFC), the startup-minded and investment-focused member of the World Bank Group, and the Bill & Melinda Gates Foundation (Al-Mahamood, 2015). Again, mobile’s lower cost-per-transaction will be an important driver to push hesitant banks to rethink their business models to remain viable in this digital world.

Like any other digital platform, M-Pesa’s glory hinged on the winner-takes-all environment derived primarily from the lack of interoperability between competing platforms through a lock-in tactic across its ecosystem. However, since the mobile banking platforms in Tanzania built an interoperability-powered mobile environment in 2014 (Robb, 2015) across several African countries, financial authorities and regulators are increasingly mounting pressure on FinTechs toward an interoperable mobile wallet regardless of their mobile networks.

This kind of interoperability is believed to foster competition while benefiting customers or the population in general. In early 2018, Kenya joined the club of countries pushing for FinTechs and digital platforms interoperability schemes, given its promising efficiency and better digital experience that can be gained across the board. However, it needs to be structured so as not to stifle innovation. That is, to design the regulatory framework by business segments such as remittance and lending in lieu of the class or category of business such as traditional banks, FinTechs, and telecom operators, according to Du’s finding in 2017.

Due to this multi-homing environment, the ease of switching between competing platforms may hurt M-Pesa’s lead in market share in the coming years. As such, Safaricom, the owner of M-Pesa, is moving into social networking to broaden its appeal. For this reason, in April 2018, the company launched a messaging app called Bonga and tightly combined it with its M-Pesa-based transactions and its users’ social networking accounts to enhance its platform’s digital experience from Kenya to Asia. Similarly, at the end of 2018, it began a partnership with Western Union to strengthen its global footprint by tapping the hundreds of thousands of agent offices of its new partner globally by strengthening its competitive edge, according to other reports.

Weak integration regarding interoperability is part of the problem, as is the aggressive monetization strategy regarding fees and the interest rate charged. In recent years across African markets, there have been serious concerns about the business model of the FinTechs, particularly in Kenya, where we have seen the rise of predatory lending, referring to unethical and deceitful actions used by several lenders to lure desperate borrowers in taking loans with exorbitant fees and interest rates attached.

In many cases, this predatory practice has resulted in outrageous annual interest rates of more than 150% in many cases by taking advantage of the poor—the financial illiterates—who face formidable challenges for credit access, said Mohammed and Fick in 2018. The main sector engaged in such outrageous practices is FinTech, particularly those startups from the West Coast of the United States that joined the party with war chests in the hundreds of millions of dollars. As a result, Kenya has responded with new regulatory measures regarding FinTechs and their lending practice in the country, noted Fick in 2018. However, the effectiveness of the measures remains to be seen.

The good news for banks and telecom operators in joining the mobile platform world is the deep insight gleaned from consumer behavior has not been seen before through analytics. Their digital footprints and habits provide rich data with an enhanced client profile from historical purchase transactions, account balance, type of consumption, stock market trading, and social media likes and comments that can be used to improve the customer experience anytime and anywhere; this is increasingly becoming the winning factor across many industries.

Certainly, for a bank (unlike the disruptors), the money required to get up to speed regarding the infrastructure upgrade during the early days of the Fintech disruption was significant. For instance, to be in the game, upgrading the backend legacy IT systems (including its associated security and compatibility issues) needed to be resolved. On top of these investments, the banking sector faced many compliance-related distractions. For example, banks on both sides of the Atlantic have been pouring over $19 billion annually on technology-related compliance issues regarding the European Union’s Markets in Financial Instruments Directive (MiFID) (Spezzati, 2017). In addition, banks neglected mobile banking by spending too much time ascertaining the cost-benefit calculus of joining the mobile bandwagon concerning the emerging segment’s profitability.

As the world moves toward the Internet of Things, our society has been fundamentally transformed. This includes the rise of eGovernment and the digitalization of government services and activities in the public sector. As a result, online public services have increased considerably in the past 15 years. For example, more than 120 countries today provide readily accessible data regarding government expenditures online to their citizens and residents. (United Nations, 2016). Also, the economy, businesses, and many other sectors have been eager to embrace the digital age. It should be clear by now that the banking industry needs to reinvent itself to thrive. However, a big problem that our consulting engagements found is that several banks are still run by “digital aliens,” who do not understand the new world we live in and are struggling to make sense of the magnitude of the challenges.

On another note, a legacy of convoluted channels such as ATMs, online banking, traditional bank branches, and remittance services distracted the banking industry (creating fertile ground for silo thinking) when functional departments or business units hoard crucial knowledge or information deliberately—and red tape. These legacy systems used to be assets in the analog world. Still, they have become serious impediments to the badly needed innovation and digital transformation to remain competitive across the sector.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.