InsurTech in FinTech Ecosystem: How InsurTech Firms Disrupt the Insurance Sector?

Since the word FinTech was coined first by the former chairman of Citicorp (now Citi Group) in the early 1990s, the FinTech landscape has evolved and become complex. However, the insurance industry’s business model has not kept pace with the rapid change. As a result, a combination of a new breed of disruptors, enablers, and intermediaries has disrupted and complemented the business model of the regulation-burdened insurance industry. This article will provide a bird’s-eye view of the disruptive InsurTech landscape, the insurance sector’s trends, and how InsurTech players disrupt the industry, including the three types of challengers and the key differences.

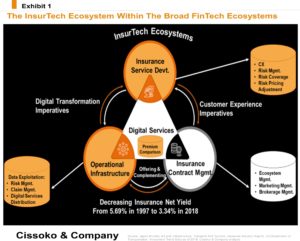

The InsurTech Ecosystem

The InsurTech ecosystem has three key pillars, and a fourth one complements others.

The insurance services development pillar is where customer experience and risk management belong, including risk coverage and pricing. The operational infrastructure pillar is the backbone of data exploitation regarding risk management, claim management, and digital services distribution. For example, this pillar allows InsurTech firms to glean fine-grained details regarding driving behavior, usage-relevant data regarding usage frequency, etc.

The granular details then provide a better picture of the customer risk. Thus, the insights allow InsurTech players to craft tailored policies based on the observed and anticipated driving behavior. The insurance contract management pillar is where the ecosystem, marketing, and brokerage management belong. The orchestration of complementary products and services, such as partnerships and other types of alliances, occurs between the three main pillars.

The Drivers of InsurTech Disruptions

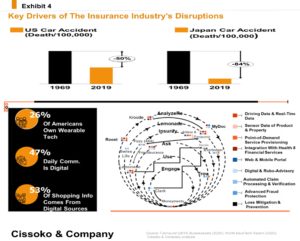

Like its mother, FinTech, InsurTech saw the light of the day because of interrelated factors. Chief among them are technological advances in recent years and demographic shifts regarding millennials and Gen Z. On top of that, the challenging regulatory environment in which insurance and other financial institutions operate stifled the needed innovations to meet the imperatives of customer experience within the industry. Consider this in the age of artificial intelligence: the players within the industry used to determine their risk calculus models when a policyholder was signing up by gathering key data; in other instances, they calculated their exposure at the time of claim processing, which looks byzantine and flawed.

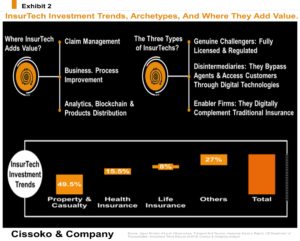

Thus, with the advances in technologies regarding artificial intelligence, data analytics, and telemetry (IoT), the InsurTech players realized that the existing business model was anything but proactive. Thus, the industry was ripe for disruption through at least three business models. The disruptors include full-stack challengers and complementors of existing services through AI, analytics, or blockchain, to name a few. The third business model is disintermediation (cutting or reducing the middleman). Moreover, people worldwide demand more with less financial resources regarding insurance policies and premiums.

InsurTech Players, how do They Disrupt the Insurance Industry?

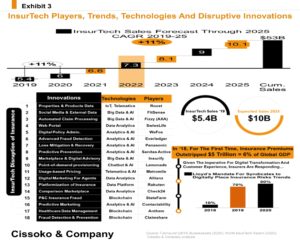

The game of the players can be categorized into three groups. That is, innovations and technologies, including how tools and delivery channels are deployed: artificial intelligence adds value by personalizing and speeding up many insurance services, IoT goes a step further by improving the quality of data exchange between various companies, predictive analytics improves risks and policyholder’s behavior in advance, which can enhance risk management and strategic decision making regarding a business segment of types of customers.

With automation trends in full swing, chatbots add value and will continue to play a valuable role in communication. Indeed, recent research predicts that by 2025, over 75% of customer interactions will be done through chatbots. Blockchain brings transparency in record-keeping and data analytics while maintaining the integrity of most—if not all—transaction records in a decentralized manner. In the same way, InsurTech players unlock value from other tools such as big data (including social media data), machine learning, and telematics, which has enhanced decision-making from reactive to proactive, given the insights gleaned. Telematics provides fine-grained details regarding airbag deployment, usage behavior, the road used by the vehicle through GPS, speed behavior, sudden braking and acceleration, mileage, and the approximate time of the day. In short, telematics provides a nearly complete picture of the consumer behavior upon which insurance policy exposure can be optimized.

The first group is the genuine challengers that are fully licensed and operate under regulations like the legacy players. In this category, players such as Roost are in the auto insurance in the United States. The second group of players is what’s called disintermediation. Through digital means, they bypass traditional retail agents to get access to customers. Disintermediation includes well-known players such as the reinsurer Lloyd’s in London. In recent years, it has doubled its digital risk placement mandates from 10% in 2016 to 70% in 2019 to 80% in 2020.

By its very nature, InsurTech comes with many risks that disruptors need to consider deeply, given the excessive reliance on data and technologies as the backbone of the business model. Our experience suggests that executives and leaders in the InsurTech industry need a strategy to tackle these 10 risks: IT, cybersecurity, fraud, business model, legal, governance, asset, data quality and privacy, and regulatory risks.

Insurance Sector’s Mounting Trouble: Falling Nominal Yields and Disastrous Losses

The average yield has fallen in recent decades. In 1997, the industry reaped 5.7% in the property and casualty segment. However, in 2016-17, the average net yield decreased to 3%, then rose to 3.34% in 2018. Overall, it is still nearly 40% below what used to be taken for granted in 1997, given the quantitative easing (QE) bazooka deployed by central banks worldwide after the financial crisis of 2008. The same downward trend holds for life insurance; the average nominal yield fell by 28% from the roaring time of 1997 to 2018. With technology-powered disruptions from InsurTech firms, the industry will have a bumpy road ahead in the coming years without crafting a sound strategic response to the emerging threats.

On top of that, in recent years, with the rising climate change-related disruption worldwide, the insurance industry has been disrupted by substantial catastrophic losses, particularly in the United States. Consider this: in 2017 alone, the industry was hit by its highest-ever losses of $104B. The following year, 2018, the industry faced another nightmare of over 47 billion in losses. All these trends point to one ugly reality: the wind of change has arrived, and the industry needs to get its house in to survive.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.