Beyond Porter’s 5 Forces: How to win the Profitability Game, and Always Smile in Japan

In companies’ search for profitability over the past four decades, the Holy Grail has been the famous Porter’s 5 Forces and his generic strategies – cost leadership, differentiation, and focus. However, firms large and small are still struggling to make decent profits in Japan and other corners of the world. In other words, are Porter’s generic strategies the only strategic options for companies in Japan and elsewhere? Fortunately, our experience suggests another option that we will discuss in this article. Through this strategy, Japanese CEOs and other business leaders will be more profitable and always smile by beating others across the value chain.

Eroding Competitive Advantage and Manufacturing Efficiency Paradox

When Japan’s economic bubble burst in the early ‘90s, the manufacturing sector began to struggle, given the rise of the Asian Tigers and enhanced competitiveness from companies in advanced economies. Consider this: South Korea’s technology powerhouse, Samsung, a latecomer to the party, overtook Sony first in late 2002. Worse still, Samsung again overtook the four largest Japanese companies (Sony, Toshiba, Sharp, Panasonic) in terms of market value in 2010.

By 2013, Samsung generated $216.7B in revenues and made a net profit of $28.8B. These developments were a testament to the fact that the Japanese manufacturing strategy, which was based on developing products rather than discovering them, hit a wall. Indeed, many well-known products, such as CDs, originated in Western countries but were developed by the Japanese. For example, in the case of the CD, Philips discovered it, but Sony was the company that developed it.

The problem with management fads is that all industries and competitors will soon adopt them. Thus, what used to provide a competitive edge will unleash a race to be an average company just like the competitor. Today, all business schools and certification bodies provide training on lean manufacturing, particularly its offshoot Total Quality Management (TQM), Just-in-time manufacturing (JIT), Six Sigma, Agile, and the like. As such, competitive advantage resulting in profitability has evaporated across industries, leaving CEOs wondering how we can survive.

The Porter Prize and the Generic Strategies for Improving Japan’s Profitability

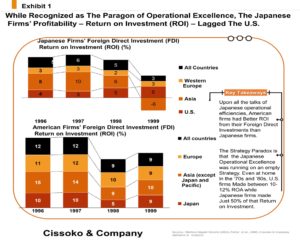

Between the ’70s and ‘80s, Japanese companies trailed their American counterparts despite all the talk about Japan’s economic miracle. While American firms made between 10% and 12% in return on assets (ROA), in Japan, firms made between 4% and 6% on their return on investments (ROA). That is, nearly 50% less than American companies. Another cold fact that Japanese business leaders realized is that the Lean Manufacturing movement does not ensure profitability as it once did.

Crudely put, Michael Porter of Harvard and Hirotaka Takeuchi co-authored a best-selling book, “Can Japan Compete?” argued that Japan must change its way. In it, they suggested that Japanese firms double down on strategy and reduce their over-reliance on operational excellence, which made them succeed in the previous decades, given that their strategies were not distinct enough.

In response, the Japan Ministry of International Trade and Industry (MITI) established the Porter Prize in 2001 to foster more strategic thinking. Like the Deming Prize, established in 1951 in honor of W. Edwards Deming, given his contributions to statistical quality control, The Porter Prize is awarded to companies with distinctiveness in their business strategies. One of the Porter Prize winners in 2019 was en-Japan’s Job ad site en-Tenshoku. If Porter’s generic strategies are not widely adopted in Japan, is there another framework to help companies find a path to profitability while smiling?

However, 20 years after establishing the Porte Prize, many companies in Japan are still struggling to find a strategic path to profitability. One reason is the lack of adoption of Porter’s strategy, as mentioned elsewhere in this article. Indeed, Porter’s generic strategies, differentiation, cost leadership, and focus have not been popular in Japan.

American and foreign companies operating in the Land of the Rising Sun use strategic analysis tools more than their Japanese counterparts. After the Second World War, many Japanese companies developed superior capabilities in Total Quality Management (TQM), just-in-time supply chain management, lean manufacturing, continuous improvement (Kaizen), and the like, which propelled Japan to the world’s second-largest economy.

As a result, there is still formidable resistance to changing these management cultures across the nation. With the loss of competitiveness during Japan’s lost decade of the ‘90s, firms began to look for the next big thing, which has yet to come. Before the arrival of the next big thing, many Japanese companies tried Porter’s generic strategies; however, the prospects did not improve as hoped. Thus, they quickly changed gears by abandoning the generic strategy altogether.

COVID-19 Made Things Worse in Japan and around the World

COVID-19 disruptions made the situation worse. Industries’ supply chains and global value chains (VGC) disruptions were a wake-up call within boardrooms on both sides of the Atlantic to rethink efficient processes such as Just-in-Time supply chains. For one thing, the lack of visibility compounded firms’ exposure to hidden and lethal risks. Because resilience was no longer an essential word in the business lexicon of many CEOs, everything seems so efficient and well-orchestrated that building resilience became a relic of the past. However, when the music stopped, business leaders suddenly realized that an optimal inventory redundancy needed to be the new game in town. Thus, the COVID-19 economic disaster accelerated discussions about digitalization while profitability strategy became even more urgent for companies worldwide.

The Value Chain’s Profitability Smile Curve

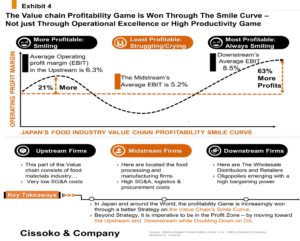

Across many industries, the midstream of the value chain generally has low profitability compared to the upstream and downstream called the smile curve—a term coined by Stan Shih, the founder and chairman of Acer Inc., a global Taiwanese player in electronic manufacturing. In his analysis of the value chain of the electronic industry, he divided the supply chain into upstream, midstream, and downstream. He plotted these parts of the value chain on the horizontal axis and the productivity on the vertical axis. Surprisingly, a U-shaped curve appeared, which looked like a smile. Hence, the smile curve.

For decades, empirical research has found evidence of the same smile curve across the value chain in Japan and elsewhere. For example, when you divide the Japanese food manufacturing industry value chain into upstream (raw material industry), midstream (food processing and manufacturing), and downstream (wholesale distributors and retailers), the smile curve of profitability appears.

The industry’s most profitable part is the downstream segment, with an average operating margin of 8.5%, 63% above the midstream. Followed by the upstream with an average operating margin (EBIT) of 6.3%, and the least profitable segment is the midstream with an average 5.2% operating margin. This part of the value chain has been under pressure for some time, given the downstream side’s consolidation, which gave the distributors great bargaining power. On top of that, the segment has a serious disadvantage because it suffers from higher procurement and administrative costs than the upstream and downstream parts of the value chain.

As such, broadly speaking, companies have three strategic choices. The first is to rethink their market entry strategies regarding which part of the value chain they intend to enter. The second one is to move upstream or downstream through vertical or horizontal integration, mergers and acquisitions, or strategic alliances.

This matters because in the midstream segment of Japan’s food industry, for example, our analysis suggests that the highest operating margin (EBIT) came from the livestock products industry, 9.7%. In comparison, the sector’s average stood at 5.2% operating profit margin (EBIT). In other words, 9.7% EBIT is what the profitability gold medalist of the midstream segment of Japan’s food industry earned. A CEO needs to ask himself: do we have a better strategy and capabilities to produce higher profitability than this? In most cases, the answer will be no.

In the worst-case scenario, CEOs wanting to join the sector can expect between 2.7% and 3.3% earned by the aquatic product industry and beverage because they are the least profitable industries in the midstream part of the value chain. Thus, if the CEOs’ strategies are based on dubious factual foundations, they can expect these profit margins at best. However, in the worst-case scenario regarding their strategy in the downstream segment, they can expect, at best, the profit margin of grocery stores at 5.7%—the least profitable subsegment of the upstream part of the value chain.

This profitability ratio is twice as high as what CEOs expect in the midstream, earning 2.7% at best when cracks begin to appear in the strategies.

The third is the defensive one, profit margin maintenance. It calls for business leaders to defend their margins by avoiding the downstream as much as possible until evidence to the contrary is found. However, given that dynamic efficiency (innovation to increase the profit pie) is what is required in the platform world rather than the competitive strategy grounded in static efficiency (firing employees, aggressive cost-cutting such as closing plants), firms with a disruptive innovation can upend the midstream of an industry’s value chain. Ultimately, they can enhance their profitability more than previously imagined.

Thus, to win the profitability game and always smile calls for CEOs and other business leaders to rethink their strategies in our increasing platform economy, which has blurred the artificial industry barriers that once shielded some firms. Business leaders need to optimize their success probabilities by considering each strategic bet’s long-tail risks of each strategic bet. In other words, CEOs need better strategic calculus to win the profitability war in this age of COVID-19. In our noisy world of shareholder activists, profitability is indeed one of the true hallmarks of corporate performance.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.