Cashless Payments in Japan and Beyond: Where to Focus to win the Game?

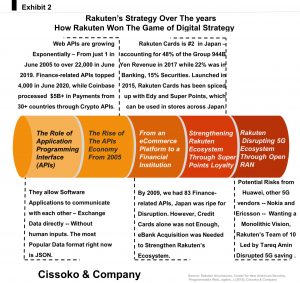

A game-changing strategy requires a game theory perspective to win the mobile payments (mobile wallets) competition in the increasingly crowded and cashless economy. The cashless landscape in Japan is very fragmented, given the low barriers to entry—not only in Japan but also worldwide. Consider this: the web APIs are growing exponentially, from just in June 2005 to 22,000 in June 2019. Finance-related APIs topped 4,000 by June 2020. For these reasons, Coinbase processed $5B+ in payments from over 30 countries through crypto APIs.

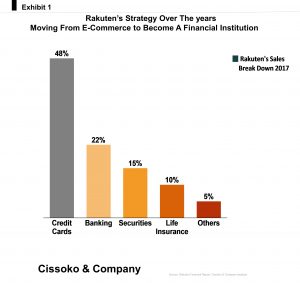

In 2009, we had 83 finance-related APIs. As such, Japan was ripe for disruption, and Rakuten joined the game. The executives at the firm knew that the credit card business was not enough. It needed to acquire eBank to strengthen its ecosystem. The strategy worked well. By 2017, Rakuten was Japan’s second-leading credit card issuer, accounting for 48% of its Yen 944B sales, while banking comprised 22%, 15% securities, 10% life insurance, and the rest of e-commerce-related revenues.

Launched in 2015, Japan’s leading eCommerce platform, Rakuten, has spiced up its credit card business with Edy and Super Points, which can be used at thousands of stores across Japan. In other words, Rakuten is a classic financial institution focused on its eCommerce business, as many still think. To be sure, Rakuten is not alone in this kind of digital transformation to strengthen its ecosystem; Amazon and Alibaba have been using the same strategy playbook for many years.

Where the Japanese Government and Payments Firms Need to Focus to win

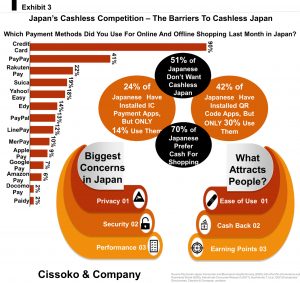

Our research revealed that 51% of Japanese people resist a cashless society growth in the Land of the Rising Sun. They see it as a disruption to their decades-old habits. Similarly, when we asked what payment method was preferred, nearly 70% of Japanese preferred shopping with cash. As a result, mobile wallet firms have spent over $181M in cashback campaigns to lure those still on the fence in recent years. The move has been a boon for the industry, particularly PayPay and, to a lesser extent, PayPal. Given the number of wallet platforms, shoppers increased by over 19% in 2019, and we expect the trends to keep growing.

Beyond resisting the cashless world, we found emerging trends in Japanese consumer behavior. While most know the mobile wallet phenomenon, many download the apps but don’t use them as expected by cashless payment companies – Fintechs. For example, while 24% of People in Japan have installed IC apps, only 14% use them as expected. Similarly, 42% have installed QR-based apps, but just 30% use them.

The three biggest concerns of Japanese people are privacy regarding the exposure of sensitive information, security regarding cybersecurity, and performance related to features, risks, and volatility of wireless communications regarding smartphones’ capabilities. However, the Japanese people are increasing their adoption of cashless payments, given the ease of use, the cashback and awareness campaigns, and the irresistible points earned from their usage.

Competitive Strategy to Reach the Critical Mass for Success

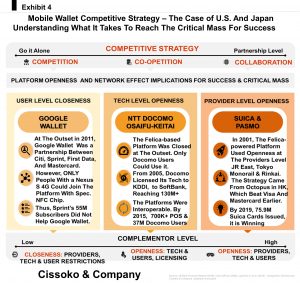

Given the fragmentation of the payments ecosystem, just a handful of Fintech firms reach the critical mass required to succeed. Our research and experience suggest that a multi-pronged strategy is required for payment platforms to become widely adopted to reach the critical mass of consumers and merchants alike.

The case studies above of Google Wallet, NTT Docomo’s Osaifu-Keitai, and Suica are illustrative, given that the clarion call for winning entails a trifecta of openness—user-level openness, technology-level openness, which can be through licensing the technology, as in the case of Osaifu-Keitai, and provider-level openness, like the case of Suica in Japan.

The Grand Strategy to win big in Japan and Beyond

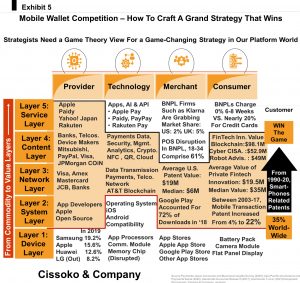

Our experience working with many platforms in the Fintech space and other industries suggests that CEOs need a game theory view for game-changing strategy in our platform world. In other words, the first step to crafting a winning strategy as a mobile wallet platform calls for layering the mobile ecosystem into its components—the device, network, system, data, and service layers.

The second step entails linking each layer to the respective ecosystem players to understand the evolving payments landscape. The third step requires filling the space with trends, market size, partnerships, M&As, and patent trends regarding innovation. Indeed, the strategic analysis seems simple, yet it is one of the most powerful strategic exercises a CEO can do for superior strategic insights across the fast-evolving world of mobile wallets. For example, the exercise revealed that nearly 35% of patents worldwide are smartphone-related.

Similarly, our analysis shows that not all patents are created equal regarding the trends in innovation and the value of innovation. For example, while the average U.S. private patent value is $52.5M and the median $9M, in the FinTech space, blockchain patents are highly valued – with the average value being $147M, followed by cybersecurity patents with an average value of $79.5M, robot advisor $73.5M.

The good news is that Fintech patents are highly valued overall—the average private value is $19.5M, and the median is $35M. These values are higher than U.S. patents on average and median counts. Another emerging trend we discovered is the growing trend in mobile transaction patents, which jumped from 4% in 2003 to 22% in 2017.

Finally, there is the insight regarding impulse payments around the world. Our experience suggests that nearly 40% of online shopping is based on impulse buying. Considering that nearly 25% of global emissions are related to the manufacture and consumption of fashion- and electronics-related products, which account for most online shopping, firms in the payments industry need to craft a better strategy to confront these cold facts.

Otherwise, critics may consider them complicit or part of the problem threatening our planet and future generations. That’s why the CEOs need a game theory view for game-changing strategy in our platform world.

Winning in the fast-changing and disruptive world of payments calls for a great strategy in Japan and worldwide. By following the guidelines religiously in this article, the payments industry and its CEOs can dramatically improve their odds of success in the years to come.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.