Digital Platform Ecosystem Strategy in the age of Disruptions

The rules of the strategy game have been rewritten. In today’s digital world, where global Fintech funding has exceeded $100 billion, where China has been leading the AI funding with the number of AI firms in the country approaching 1,500, where Apple made nearly $20 billion in digital goods sales in 2019—roughly 30% of the almost$63.5 billion sold on iPhone and iPad combined. As a result, it surpassed briefly a market capitalization of $1 trillion in August 2018. The growth did not end there. The company reached a major market cap in the summer of this year (2020)—a milestone of topping $2 trillion. So, the conventional wisdom of the old order of strategic management is becoming an increasing liability for firms.

Knowing how strategic thinking has evolved in the digital age is imperative to succeed in this new digital platform environment. Moreover, this strategic thinking shift has been compounded by COVID-19, where volatility, uncertainty, and ambiguity are the new normal; firms have a choice to embrace this new reality or resist it at a prohibitive cost. Indeed, the proliferation of multisided platforms (MSPs), the data-powered and digital-experience-centric firms that smooth communication and contractual agreement between different parties, among others, have shifted the paradigm and challenged many assumptions of traditional economics familiar to many executives and business leaders.

Consider Fiverr’s platform connects sellers (freelancers) to people who need freelancers, such as graphic designers and coders. So, the demand for these freelance services depends on people like you and me who need such services. Similarly, the demand from you and me depends on people willing to provide freelance services.

In other words, the more people who need freelancing, the higher the number of freelancers on Fiverr’s platform and vice versa. So, Fiverr, in its early days, had to deal with the so-called chicken-or-egg challenge of whom to attract first between these two sides (freelancers and people who need freelancing services), and how? The company needed to decide whether it should charge both sides of the platform users or just one. So, given the value creation and capture dependence on each ecosystem member regarding this business model—analyzing the multisided platforms (MSP) like the legacy businesses (one-way value creation) through textbook economics will be flawed.

The leap of Internet communication technologies in the past decades has triggered a strategy and paradigm shift that digital platforms seized on to deal effectively with economic frictions that had plagued our economy for some time. For this reason, the financial market rewards them with handsome dividends. Indeed, platforms are dominating the economy with their meteoric growth and stratospheric valuation. A growing body of anecdotal evidence illustrates the point. In 2015, Airbnb was reportedly valued at nearly $25 billion, given sales of more than $845 million (a revenue multiple of almost 29.5) with almost no inventory whatsoever. Marriott, which had nearly $14 billion in sales and managed more than 4,000 hotels, was valued at almost $20 billion, a revenue multiple of 1.5. That is a huge difference.

Today, many top brands are MSPs, including familiar household names such as eBay and Rakuten and many of the leading startups and social networking sites, such as Lyft, Uber, Airbnb, Twitter, WhatsApp, Viber, Line, Meetup, Flipkart, Upwork, Reedsy, 99designs, and Freelancer. This club includes credit card giants such as Amex and JCB in Japan.

The Drivers of the Platform Ecosystem Model

The main drivers of the platform model and its ecosystems are the costs associated with infrastructure and advances in technological processing and storage capabilities. In most advanced countries, we estimate that the Internet transit price for megabits per second has decreased on average by 33% yearly over the past two decades and is approaching zero.

Marc Andreessen (2011), the leading venture capitalist, suggests that the monthly infrastructure costs have decreased by a whopping 99% within the 11 years through 2011, thanks to Amazon Web Services (AWS). Other noteworthy drivers of the MSPs are the proliferation of various classes of software—the Internet of Things (IoT) (through its enabled connectivity) and its sibling Industrial Internet of Things (IIoT) (through its data-powered electronic devices)—including smart meters for energy consumption data analysis and communication. Also, sensor-powered yield monitoring devices for enhancing farming productivity are under the umbrella of IIoT.

To succeed in this platform economy, companies need a strategy based on a combination of innovation, technology, talent, and data to deliver value not solely to one side (stakeholder) as in legacy businesses (focused on an end-user through a one-way street traditional value chain), but to many sides, such as platform users, content creators, and software programmers. And this value cannot be created alone. So, the focus has shifted to coordination while discouraging rigid systems of control as in the analog era. We discuss this point further in the following section.

Education Platform Ecosystem Strategy in the age of Disruption

Over the past few years, the new education game in town has been the MOOC through platforms such as Coursera, Audacity, and Edx, among others. Moreover, the coronavirus pandemic has accelerated the move to online education, given the risk associated with face-to-face classroom interactions. As such, we anticipate that the competition among online education providers—incumbents and new entrants—may become increasingly intense regarding the business model that firms will choose.

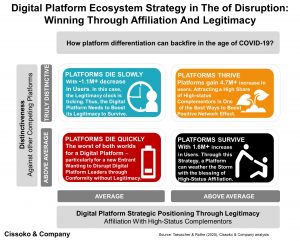

The big question is: How can organizations that want to compete in the education platform ecosystem win through a better business model? Our experience, consistent with the latest research on the subject, suggests that the legitimacy of the education platform is the key. That is, being affiliated with the institutions (complementors) with a golden cache separates the winners from the rest. An educational platform with a high share of high-status universities (complementors) on its platforms has increased its users by more than 4.7 million. As such, when an organization or would-be disruptor has this kind of legitimacy, it can differentiate itself by becoming an anti-conformist without being penalized by the stakeholders. However, when a “wanna-be” disruptor goes very far from the acceptable standards in the industry through its distinctiveness without a top-notch affiliation under its belt, the maverick move can penalize the firm through a huge loss of its platform users.

Indeed, our findings suggest that the maverick disruptor in its quest for high distinctiveness (differentiation) from the norms and beyond the acceptability range within the education platform ecosystem can backfire through a huge loss of its platform users—more than 1 million will jump ship to join a rival platform. Because contrary to digital platform ecosystems in other industries, the education sector is an outlier. Thus, organizations need to understand these key differences to avoid the pitfalls that have disrupted many would-be disruptors who have committed strategic suicides in this industry on the cusp of disruption and pregnancy for change.

To weather the COVID-19 pandemic storm through resilience, organizations need to combine both platforms, which are the average platforms, regarding differentiation. However, they strive to attract complementors (educational firms or teachers) with high status – those with established credibility across the educational sector—to reach the critical mass necessary for the positive network effect cycle. Our experience suggests that a firm using this platform strategy can increase its users by more than 1.6 million.

However, the worst of both worlds is to be an educational content conformist while having average or below-average high-status affiliation with more credible institutions around the world as partner complementors. In this situation, the “wanna-be” disruptors will die quickly. Therefore, the disturbing fact is that a winning digital platform strategy in the education sector entails understanding the complexity of the hard-nosed practical challenges mentioned in this article. We believe this is the clarion call for vigilant organizations.

For more on strategy, organizations, and the coronavirus, please read our collection of insights regarding COVID-19, building resilience, and a winning culture for the age of disruption here.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.