Platform Ecosystem: How Strategic Thinking has Evolved in the Digital Age?

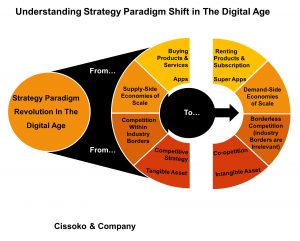

Firms must learn to change to earn in the digital age because value creation has shifted from supply-side economies of scale to demand-side economies of scale (i.e., positive network effects). By now, the message regarding the new strategy rule should be loud and clear for all forward-thinking firms: In this platform age, the extent of a firm’s network is correlated with its real worth. Indeed, over the past five decades, the average lifespan of S&P 500 companies has shrunk to less than 20 years. Therefore, this should be a wake-up call for strategists.

Moreover, when it comes to valuation and resilience in the age of COVID-19, intangible assets trump tangible ones; the open platform model quashes closed ones. Today, the top firms by market capitalization are increasingly in the tech sector. These data-powered firms use roughly 12 times fewer employees than their counterpart legacy businesses. They are valued higher in market capitalization than the larger manufacturing companies in their heydays of the industrial organization era. The big question is this: What does this mean for your strategy? In the following sections, we have listed some, though not all, of the strategic paradigm shift from the old order to the digital age. Below are some of the essential strategic paradigms of revolution in our robot age.

From Industry-Focused Analysis to Borderless Industries

In truth, industry analysis in the past decades yielded mixed results for strategists. However, since the artificial boundaries between industries have been falling in recent years, with disruptors and challengers rising from all regions and adjacent sectors, industry analysis simply no longer works. Uber, Amazon, Tencent, and Airbnb epitomize the disruptive power of the well-touted digital platforms.

Crafting a strategy solely on your industry and your current competitors is a path to ruin and disappointment. Defending your position within an industry over time may seem like a fool’s errand. Constant reinvention—not defending the status quo—is the way forward in our fast-paced environment. Indeed, 30 years ago, in 1989, to be precise, one of the world’s foremost strategy experts—the late Bruce D. Henderson—the founder of Boston Consulting Group (BCG) warned that over-reliance on market share is nonsense. In other words, a single-minded focus on this measure alone is woefully wrong and can spell disaster down the road.

Consider this: Japan Airlines (JAL), in its aggressive quest for market share, got the coveted title of Asia’s largest airline by sales. At home across Japan, the same market share quest led the firm to many inefficient routes—arguably, to please many Japanese politicians. What happened next? Well-touted Asia’s biggest airline filed for bankruptcy protection in January 2010 with a debt load of over $20 billion. In contrast, Apple accounted for less than 23% of the global smartphone industry revenue in 2015. However, it earned more than 85% of the industry’s profits. So, the way forward is to use a profit pool, not market share, to avoid embarrassing bankruptcies in this digital age. These developments were a severe blow to the misguided conventional wisdom of strategy based on just acquiring market share, particularly in mature industries. There seemed to be a relationship between market share and profitability, so many executives still believe they should prioritize market share as the top strategic key performance indicator.

So, from this misunderstanding of the relationship between these variables lies the dangerous practice of equating market share to profitability. A correlation exists between them, but not causation. Also, as the boundaries between industries are becoming nonexistent in our networked world, these previous relationships between market share and profitability are increasingly getting harder to prove. There are many frameworks in management, such as the service-profit chain, with the causal relationships overly generalized by their proponents. According to the more recent literature, the relationships have been sold as universally applicable, which is not the case. Indeed, given that these types of frameworks were built with a one-way street business model in mind—as explained elsewhere in this article—their applications will be unfit for the digital platforms with their ecosystems-based models and two-way street value creation process. In other words, the aforementioned causality-inspired management frameworks are deficient in business models where value creation and capture mutually depend on the entire ecosystem.

Again, where this relationship rings true, the conditions a firm must meet to apply the model and get results may need clarification so businesses do not burn their fingers. Consider this: The Japanese insurance company Fukoku made redundant more than 30 of its employees with an AI-powered IBM Watson to save costs in the first week of January 2017 alone while hoping to increase its productivity by more than 25%. With machines replacing humans projected to reach more than 4.8 million this year (2020), we wonder how models, such as the balanced scorecard and other similar deterministic models, will still be helpful, given their underlying assumptions. Since machines are increasingly replacing employees, they are the linchpins of those models.

As all researchers know, there is a difference between internal and external validity regarding research. Indeed, equating market share to profitability is an illusion. So, blindly using market share as the sole key performance indicator (KPI) is unfortunate but dangerous in this new age of drones, smart homes, and smart factories. In fact, our experience points to a better gauge than the market share; when you think it is necessary (use the sector profit pool), assuming you still believe that your sector or industry under analysis has an artificial boundary—the combined profit pie along the value chain. For example, in the automobile sector over the past decades, the finance-related segments have consistently been the most promising and profitable segments with double-digit returns on sales, while the core manufacturing and dealership languished with razor-thin single-digit returns.

From Products Competition to Ecosystems Competition

Before the platform age and software embedding technologies, the game used to be product versus product. However, today, having a stellar product alone is not enough. What is salient right now is a firm’s ability to use digital technologies to facilitate business transactions or social interactions between different value-creating and value-capturing sides by solving the economic friction equation. As such, the firms that have mastered the facilitation game (by harmonizing the badly sought-after transactions and human interactions) will grow exponentially beyond their wildest dreams. For instance, it took Facebook and Google just a few years, around 60 months, to reach a revenue of $1 billion (which was pretty much unthinkable decades earlier) compared with decades for most traditional businesses.

Platforms, particularly those that have reached critical mass, grow quickly like wildfire, and are valued higher than traditional legacy businesses. That is why a growing number of business leaders are pressing their boards to get on the bandwagon. Recent studies have found that the average revenue multiple of the network-powered firms is slightly shy of 10 times, while legacy models are, on average, valued below four times their revenues.

For example, during its acquisition in 2014, WhatsApp had around 30 engineers serving nearly half a billion users. Its secret was that it used a decades-old coding language known as Erlang, which enabled the upstart to deal effectively with millions of concurrent chats with almost no downtime. For this reason, the app could scale faster with fewer employees, reach new markets, and disrupt its competitors in ways not previously imagined. In addition, platforms have near-zero marginal costs, while legacy firms still have high marginal costs to be worried about.

Platforms have defied the old presumption of economics textbooks by selling their products, in many cases, below the so-called marginal costs. Given that, unlike the traditional businesses competing for supply-side economies of scale, the platforms compete to enhance the other side of the economies of scale—the demand side.

Digital firms believe selling below the marginal costs is part of the solution. For this reason, when facing the so-called chicken-or-egg problem, which side of the platform must first be attracted? The answer, for many, entails subsidizing one side of the platform to attract and deliver value to the whole ecosystem. By doing so, digital firms make money on the asset side. For example, Facebook and LinkedIn platforms lose money on developers while they make money from advertisers and professional job seekers, respectively.

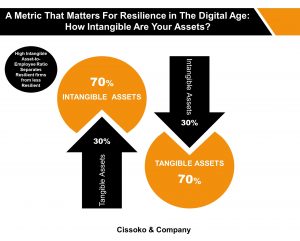

Finally, there is a dramatic shift toward intangible assets, patents, brands, software, employee engagement, and so on regarding business valuation. Back in the ’70s, intangible assets comprised nearly 15% of the value equation on the S&P 500. However, as of 2015, they constituted almost 90% of the firm’s valuation. So, given that digital platforms have traditionally focused more on intangible assets, their valuations have skyrocketed in recent years. Their strategy has focused on market values concerning intangible assets, while legacy businesses keep investing in physical assets, which are becoming less important today. Indeed, during this COVID-19 Pandemic, organizations with business models that rely least on their workers for productivity have beaten the companies with labor-intensive operating models by nearly 40% on the S&P 500, according to the findings of Deluard of StoneX.

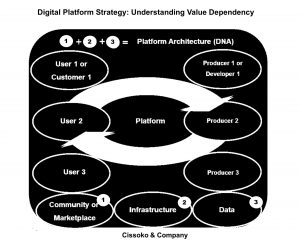

From end-user Value Focused to Ecosystem Value Creation

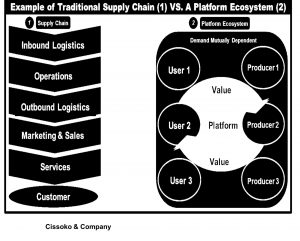

In the traditional business model, value creation and capture have followed a pipe-like pattern: The value creation starts from procurement to manufacturing, from distribution (with sales in between) to the end-user (customer). This is a classic one-way-street business model, where the value creation model is not interdependent; however, across the platform ecosystem, the major role of the platform (such as Twitter) is to enhance the smoothness of the concurrent communication and mutual digital experience of the whole ecosystem. In other words, value is created differently, given that it is interdependent on all stakeholders

The platform model uses a collaborative approach for delivering outstanding mutual value to all stakeholders, such as the platform proprietors (Facebook in this case)—the users (me and you)—the third-party coders, or other content creators. However, this is not just for a narrowly defined customer segment like the legacy business models, where firms focus single-mindedly on the customer or at least one type of customer—just one stakeholder, among others. We are not suggesting that focusing on a customer segment is a bad thing; instead, we are contrasting the value delivery model of these two types of business models.

Focusing only on the interest of just one stakeholder, such as the platform proprietor, while ignoring the other stakeholders will hinder the scalability concerning the critical mass needed to sustain the positive network effects of the platform. Two classic examples are Myspace and Blackberry networking platforms. In the case of Myspace, when Rupert Murdoch’s News Corporation acquired the site, the priority switched from the platform ecosystems’ value creation to Myspace’s self-centered value creation with a misguided monetization strategy and illusory sales target. As a result, user dissatisfaction ensued, and many moved to Facebook while Myspace lost its luster.

Similarly, in Blackberry’s case, the leadership failed to grasp that the strategy game had changed. They were slow to learn and adapt to the new platform ecosystem game in town. The firm’s executives thought that someday and somehow, the ecosystem game would revert to a product game where the firm had a competitive edge. Blackberry’s failure was, among other things, the result of a lack of strategic agility. That is, adapting swiftly before the disruptive impacts on earnings become a full-blown crisis or imminent bankruptcy. As we all know, success breeds complacency, and before the new imperatives of the ecosystem game were understood, it was too late for Blackberry.

Strategy across industries calls for a fundamental rethink. To win in the age of the coronavirus, it is imperative to understand first how disruption works in the 21st century for better responses to COVID-19. Second, how to build organizational resilience by capitalizing on $700 billion opportunities. Third, how to lead with purpose by revamping toxic corporate cultures in the age of COVID-19. Fourth, how to build an effective corporate culture to tackle the challenges of COVID-19. Fifth, how to develop CEOs’ strategy IQ to deliver a gold medalist’s performance. Six, we believe that CEOs need to master the strategy tools and techniques for pre-emptive and defensive strategies in the age of COVID-19. Seventh, crisis leadership, how to develop a new digital vision for the age of disruption. Eighth, beyond agile teams, how to build resilient teams.

In our experience, firms that understand the strategic thinking shift in the business world today and follow the steps above will thrive during these economic storms worldwide.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.