FinTech Disruptions of Asia Banking: FinTech Competitive Landscape Report 2022

The stability and business model of the banking industry has remained mostly unchallenged since Banca Monte dei Paschi di Siena was launched in 1472 in Italy. Since 1838, most financial transactions have been carried out by telegraphs.

The greatest innovation in our modern age was the launch of ATMs by Barclays in 1967 (“See FinTech innovation trends over the past 55 years”). However, over the past decade, through the rise of FinTech disruptors and other digital challengers, the pillars of the banking sector’s stability and business model have begun to crumble.

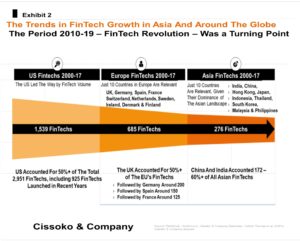

The key drivers of FinTech firms’ growth are, on the demand side, changes in demographics, trust in Tech as solutions to more modern issues, unmet customer needs and changes in customer value and preference. On the supply side of the equation are the promise of technology, changes in the regulatory environment, such as the European Union’s Second Payment Directive (PSD2), inefficiency in the banking sector, legacy IT infrastructure, and competition within the financial sector, among others. For these reasons, from 2000 to 2017, the number of FinTechs jumped to nearly 2,950, with American FinTechs accounting for the lion’s share of 1,539 FinTech startups launched (over 50%), including 925 launched in recent years.

Global FinTech trends of the past decade—2000-17

From the early days of the digital age (after the dot.com bubble burst), Fintechs emerged without visibility and the acronym FinTech (Financial Technology). The financial crisis of 2008 was a turning point when Bear Stern, the New York-based global investment bank, securities, trading, and brokerage, failed and sold to JP Morgan. This unprecedented panic sent shock waves around the globe. Given that Bear Sterns and many other financial institutions were deeply engaged in securitization and issued large volumes of asset-backed securities, these revelations and their consequences on the value of real estate and other related assets were a watershed moment.

To respond to the 2008 financial crisis, central banks worldwide deployed quantitative easing (QE) bazooka. The United States Federal Reserve’s balance sheet increased from $1 trillion in 2007 to $4.4 trillion in 2016. Similarly, the European Central Bank’s (ECB) balance sheet ballooned from $2.1 trillion to $3.5 trillion during the same period. Furthermore, the Bank of Japan (BOJ) deployed its monetary firepower by enlarging its balance sheet from $1 trillion to $4.1 trillion. The Bank of China followed suit with its aggressive defense of the financial system by increasing its balance sheet from $5 trillion to $17.3 trillion over the same period. Combined, the world’s four leading Central Banks enlarged their balance sheets by more than 210%, given the magnitude of the 2008 crisis.

The growing distrust of the financial industry, compounded by technological advances, such as artificial intelligence and big data analytics, including the launch of the iPhone a year earlier, provided a fertile ground for FinTechs to launch their disruptions of the banking and financial sectors of the global economy. Between 2008 and 2016, the number of FinTechs nearly doubled. By the end of 2017, the number of FinTechs across the leading regions reached 2,951—with the United States at the top of the list with 1,539 FinTechs, followed by the United Kingdom in a distant second position.

The growth of FinTech startups by region has been skewed toward more developed countries than emerging economies. The US alone produced over 1,500 FinTechs over 2000-17, while Asia managed to produce just a few, around 276 FinTechs—compared to the EU, which produced 685 FinTechs.

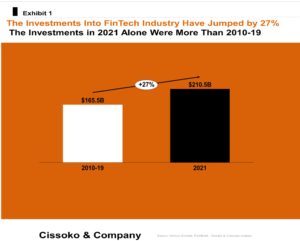

With the disruptive promise, value, and efficiency FinTech firms can unlock, investments have been pouring into the sector like never before. During the FinTech revolution – 2010 to 2019—the money invested in the FinTech sector was $165.5 billion. With the COVID-induced digital transformation and stay-at-home orders worldwide, in 2021 alone, global investments into the industry crossed the $210 billion mark—27% more than the so-called FinTech revolution period of 2010-2019. Consider this: the payment segment alone during the FinTech revolution period (2010-19) received over $90 billion in investment, with over 760 successful exits, more than 550 acquisitions, and 210 IPOs. For example, PayPal acquired iZettle in 2018 at a price tag of $2.2 billion.

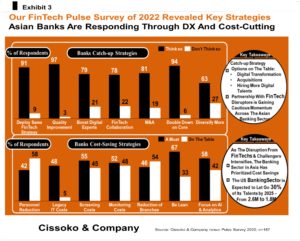

The strategic and innovative moves (including milestones) of the Fintech disruptors such as payments startups, mobile wallets, InsurTech, RegTech, robo-advising, and, lately, blockchain, make headlines worldwide regarding fundraising from venture capital fund (VCs) to private equity and corporate VCs. Our Asia pulse survey tried to uncover the key question of how the Asian banking sector responds to FinTechs and other digital challengers.

How the Asia Banking Sector is Responding to the Threat

Given the regulatory constraints and legacy IT hindrances, the Asian banking sector has doubled down on a three-pronged strategy:

• Digital transformation acceleration

• Aggressive recruitment of digital experts, and

• Cost savings across the business models

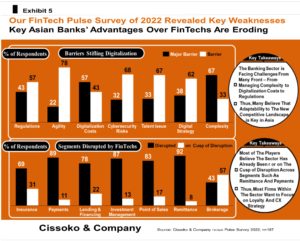

Given the threat posed by FinTech disruptors, managing the cost-to-income ratio is becoming a top priority. For one thing, banks’ profitability largely depends on managing key operating costs well, such as employee remuneration quality of asset management by bank branch managers. Consider the cost of Know Your Client (KYC): Thomson Reuters found that in the financial industry, companies spend between $60 million and $500 million per year to be up to date in complying with the demand. Thus, according to the respondents, it is widely believed that doubling down on relevant FinTech technologies can make a huge difference in profitability, considering cost reduction potential.

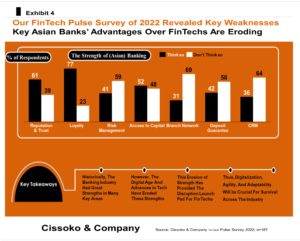

Moreover, while access to capital was one of the industry’s key advantages, many executives’ fates have been shaken in recent years. However, in other aspects of the banking game, such as risk management, branch network, and deposit guarantee, most players in the sector think that those traditional advantages are eroding, given the rise of digital alternatives across the board.

The Most Disrupted Segment of the (Asian) Banking Sector

According to recent years’ daily experience and perception, most respondents believe that six segments are under the cusp of disruption and becoming increasingly competitive – through margin erosion. They include banking segments: payments, remittance, lending and financing, point of sales, investment management, and brokerage.

At the top of the list is remittance, where 92% of respondents believe it has been disrupted, followed by payments, said 89%, and in the third position, just below the second, is investment management, said 87%.

Since FinTech startups are increasingly attacking the most profitable segments of the banking sector, the banking industry needs to respond faster to confront the threat before it’s too late. In fact, in our digital age, speed separates the winners from the pack, according to our experience. Indeed, according to our research, Fast strategic decision-making boosts sales by 38% and profitability by 42%.

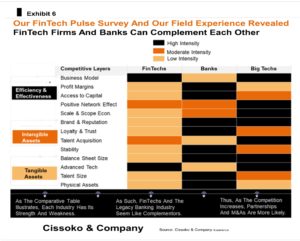

Beyond Asia: FinTechs Versus the Banks Versus big Tech

Given FinTechs’ splash-making power, their names make glowing headlines for whatever reason, from fundraising to joining unicorn clubs. However, the tech-savvy and asset-powered big tech firms (digital platforms), such as Apple, Amazon, Japan’s leading eCommerce firm, Rakuten, and Alibaba, are serious players in the FinTech space. Indeed, like other Tech companies, Rakuten is increasingly becoming a financial institution through its position as Japan’s leading credit card issuer by purchase volume.

In fact, the European Union Second Payment Directive (PSD2) opened the banking industry’s doors to third-party players, including many technology firms, through financial APIs (application programming interfaces). Banks are now obliged to share some of their key competitive advantage customer data.

Thus, big tech firms and digital platforms do not play the traditional rules of textbook economics; instead, they are data-powered firms that win the competitive game through their vast ecosystems cemented by positive network effects. In other words, the more people join and behave well by playing by the platform’s rules while adding value, the more these interactions and content make the platforms more valuable by attracting others.

Given these built ecosystems over the years, they grow faster than other competitors, lacking such vast ecosystems powered by positive network effects. For these reasons, in just a few years, Alibaba’s Ant Financial (previously Alipay) won nearly 50% of China’s market share, a 432 trillion yuan mobile payment market in 2021.

Armed with powerful digital platform ecosystems, Apple, Amazon, and Google compete aggressively for payment market share. Apple had over 265 million users globally; in Europe, 3% of people who used smartphones in 2017 purchased through Apple Pay. Similarly, in 2016, nearly 1% of smartphone users used Google Pay, equivalent to almost 2.3 million people. Furthermore, 6% of Facebook users said they used its payment within Messenger, equivalent to more than 19 million people who used the app for payment once a week in the United States alone that year. Furthermore, as previously discussed, beyond technology, Samsung and Apple use this competitive strategy to beat competitors like a joke.

In short, we believe that banks and FinTechs are complementary, given that the strengths of FinTechs are the emerging weaknesses of banks. That’s why, in recent years, partnerships and collaboration have grown within and across the industry in India. For example, recently, Axis Bank partnered with FinTech Fast Cash, and FinTech Credit Mantra has teamed up with the Bank of Baroda. Beyond partnerships, we anticipate more mergers and acquisitions (M&As) beyond the benefits of collaboration.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.