FinTech Innovation Trends Over the Past 55 Years: How Valuable is Your Innovation?

Before being coined Fintech in recent years, financial technology has a long history going back to 1967 when Barclays Bank launched the first ATM. A few years later, BACS and CHIPS technologies were launched between 1968 and 1970. They were followed by SWIFT technology in 1973, which allowed financial institutions and banks to send and receive financial transaction information quickly and securely. In this article, we will deep dive into the Fintech ecosystem and provide CEOs and entrepreneurs a guide to valuing and strategizing about FinTech innovations, given the value of each vertical innovation patent (Exhibit 4) based on our experience consistent with recent research based on innovation data spanning 15 years—2003 to 2017.

In 1999, Japan’s leading telecom provider, Docomo, launched Osaifu-Keitai (mobile banking), allowing users to do basic mobile banking through SMS. By 2004, in partnership with Sony and Sharp, Docomo launched an NFC-powered mobile banking service through FeliCa.

The year 2007 was a key turning point, given the launch of the iPhone and the brewing financial crisis of 2007-2009. During that time—in 2008, to be precise, blockchain was launched, which added great hope to the promise of FinTech. Finally, in 2009, when Bitcoin was launched as a cryptocurrency, it fueled the euphoria.

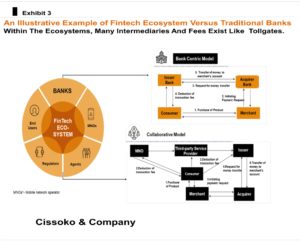

One of the emerging powerful technology layers of the FinTech ecosystem is blockchain. However, many still confound this distributed ledger with cryptocurrencies. Indeed, blockchain has more profound applications beyond crypto, including trade finance, parametric insurance, real estate transactions, settlement, and OTC derivatives markets clearance, among others.

Similarly, big data analytics and automation are gaining ground within and across the financial industry. Moreover, artificial intelligence applications are increasingly deployed on unstructured and structured data to glean insights regarding the creditworthiness of consumers, risk management, fraud detection, and consumer behavior for strategic decision-making and corporate performance improvement.

Advances in Tech Made Disruption Likelihood Very High

A few years ago, the banking and financial institutions invited disruptors——FinTechs——their shores by neglecting a huge portion of the population and businesses. That’s one of the reasons from the onset of the financial crisis of 2008; FinTechs, such as M-Pesa in Kenya, Revolut in the United Kingdom, and Klarna from Sweden, to name a few. In the United States alone, over the 84 months through 2017, 40 FinTechs were launched every month. One of the reasons behind this growing trend is the unmet needs across the board. For example, in 2019, 45-55% of small and medium-sized companies did not have an overdraft allowance, according to the International Financial Corporation (IFC).

FinTech startups have focused their efforts on the most profitable financial industry segment. As a result, the return on equity (ROE) has been eroding in recent years. Beyond traditional FinTech startups, giant Tech companies have joined the bandwagon, from Amazon to Apple to Rakuten, including Alibaba. Consider this: in less than five years from its launch, Ant Financial managed assets of $211 billion.

Unmet Needs Inviting Challengers Across the Sector

Nearly 45% of small and medium-sized firms’ lending applications are rejected in the United States. Similarly, over 29% of smaller loan applicants in the United Kingdom faced the same fate as their American counterparts. There is an estimated funding gap of $65 billion. Thus, these unresolved problems have created huge opportunities for FinTech startups to launch attacks as disruptors or challengers of the traditional financial sector.

For these reasons, pressure is mounting on the financial industry to adapt as much as possible to survive. Indeed, Citigroup estimates that over 29% of personnel in the banking sector must be reduced in the United States alone from 2.6 million to 1.8 million within three years through 2025. Owing to the digital-powered processes from which FinTechs derive cost savings and, ultimately, competitive advantage.

Venture Capital Investment Trends in the FinTech Sector

The venture capital world has poured money into FinTech over the past decades. In 2021 alone, a whopping $210 billion was invested in the sector for over 5,680 deals, with traditional venture capital funds (VCs) accounting for more than $114 billion while corporate-run venture capital accounts for over $49 billion.

Through this investment noise, the Buy Now, Pay Later segment saw a huge boost, including PayPal’s acquisition of the Japan-based Buy Now, Pay Later startup Paidy by PayPal for a reported $2.7 billion. Moreover, globally, crypto and blockchain have attracted huge investments of over $29 billion combined. All these trends suggest that FinTech disruptions are here to stay for good.

Unlocking Value Through FinTech Innovation Strategies

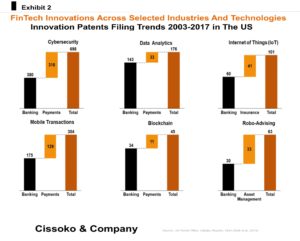

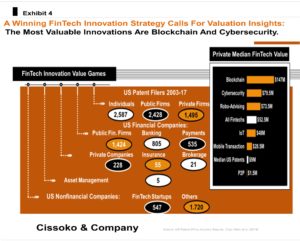

The problem with the trends above is that they miss many hidden trends that characterize genuine innovation patent value or innovation within and across sectors. For example, a 15-year data analysis of US patent filings suggests that over 6,000 patents from various industries were filed from 2003 to 2017 across many technology categories that underpin the FinTech value games.

To win and unlock the huge potential of FinTechs, companies, CEOs, and entrepreneurs in the sector must know where innovation value truly lies. By gaining such insights, banking, payments, and blockchain firms can craft winning innovations that provide bang for the buck; otherwise, misguided innovation strategies abound. This is particularly crucial with rising inflation, stock markets tumbling, and a rising discount rate environment.

The data revealed that blockchain provides the highest value for innovation patents at $147 million, followed by cybersecurity with $79 million, and robo-advising taking the third position with an estimated $73.5 million of patent value. The median value of all Fintech innovations is $52.5 million across all technology categories. Among all FinTech innovations, the P2P is the only one providing value below the median United patent value of $9 million in 2022.

To be sure, the FinTech world is fast-paced and constantly evolving. Like other industries where innovation is necessary to thrive, entrepreneurs and business leaders need an innovation strategy to create, capture and unlock value across the FinTech ecosystem. Since money will become a scarce commodity in this emerging business environment and many private firms’ valuations will go down, knowing where to focus your scarce resources will separate the winners from the pack.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.