Payments Platforms Competition: Why Docomo Disrupted Mobile Payments?

The mobile payments industry is one of the most fragmented sectors worldwide. Most players compete to provide a better customer experience through QR-based codes or NFC-related technologies. The two key questions are: Why has the industry not agreed on a technology architecture standard for the entire industry? Why and how did NTT Docomo disrupt the global payments industry? A granular understanding of these mobile wallet industry insights will allow CEOs to craft a geographically dominant payments architecture strategy that enhances their likelihood of winning.

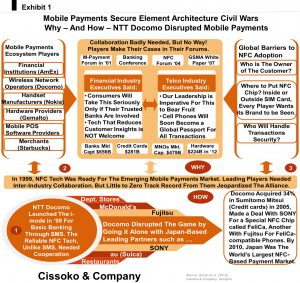

NTT Docomo was (and is still) the leading telecom company in Japan and has the largest market share. It became the leading pioneer of mobile payments technology through its i-mode. In 2003, Japan had over 61M mobile internet users, with nearly 14% using a 3G network – making the country a fertile ground for anything mobile commerce (m-commerce) instead of traditional computer-based commerce.

Launched in February 1999, i-mode, the portal-based technology, allowed basic banking operations through a mobile phone SMS – combined with a bundle of products such as entertainment. However, compared to the emerging technology called Near Field Communication (NFC), the i-mode was archaic, given its underlying portal-based technology and the small amount of money people could use at the time.

The emerging and competing technology at the time, the NFC, was based on radio frequency technology that communicates with the point-of-sale reader through the help of chips inserted within mobile phones. The reader at merchant sites is linked to a financial institution or a credit card firm-controlled payments platform. Thus, consumers could buy whatever they want with mobile phone-powered NFC by holding their phones against merchants’ NFC-tagged payment checkouts.

Big players in the Japanese banking sector, such as Sumitomo Bank, Sakura Bank, Fujitsu Limited, and Nippon Life Insurance Company, responded by launching a neo-bank called JNB. It operated solely online without a bank branch but offered time deposits, money transfers, and savings accounts, among other services. People could withdraw cash at over 90,000 ATMs across Japan.

With the rise of mobile phone adoption in Japan, with over 1,300 i-mode compatible sites and counting, pressure mounted on Japan’s traditional banking sector to adopt mobile channels. As a result, Mizuho, Mitsui Sumitomo Banking Corporation, and UFJ (now part of Mitsubishi Financial Group) became aggressive, given the opportunity for cross-selling and building customer loyalty across the Japanese banking market.

The major barriers to the NFC-based mobile technology architecture standard

Three major hurdles disrupted the cooperation between the major players and industry stakeholders. The first one is the customer relationship issue. They could not agree on which player or industry would optimally handle CRM management.

The second is security-related disagreements between telecom industry players and the banking industry. While the banking sector wants time-tested security protocols and modules, the telecom sector thinks otherwise. Instead, they proposed a single-wire protocol, which the banking sector disliked.

The third hurdle was the risk aversion regarding the mass production of (subscriber identity module) SIM-centric phones from handset makers, given the uncertainty associated with the mobile market architecture standard. As such, the uncertainty, lack of commitment, and unending disagreements led to a vicious cycle of doing nothing

Again, they could not agree on where to put the SIM card. That is, to have it inside the mobile phone (the choice of the telecom sector) or outside the mobile phone (the choice of the banking sector and want their brands to be seen by customers). Understandably, the SIM card-based secure element has become the popular choice of mobile network operators (MNOs). The SIM card will store relevant information for authentication and identification of a specific user on the MNOs’ network. As such, the SIM-centric secure element gives more customer relation power to the MNOs.

As interdependence shows, adopting a mobile technology architecture standard for payments and mobile banking requires inter-industry and intra-industry cooperation—even collaboration—through the broader value chain.

However, consistent with empirical and contemporary evidence, dominant players in their respective industries have a poor track record in intersectoral cooperation in reaching agreements. The emergence of mobile payments with the convergence of the financial and telecom industries makes cooperation grounded in a win-win agreement imperative. That is, players in banking, handset manufacturers, software makers, merchants, banks and financial institutions, and technology providers, among others, need to work together to benefit the payments industry.

While the payments sector needs more cooperation, key players in their respective industries and associations have wasted years trying to influence the mobile payments architecture in a way that will benefit them more than others. Similarly, the lack of experience working together is part of the problem, resulting in a trust deficit among leading players.

Given the interdependence of industries and players, one should expect more win-win agreements. However, this was not the case until 2004. That’s why NTT Docomo disrupted the industry through a coalition of Japanese firms such as Sony and Sumitomo Mitsui Cards.

To be sure, being the first mover alone is not enough. Winning the mobile architecture battle entails building a strong coalition for action. More than a decade after the emergence of NFC technology, the industry still can’t agree on a global payment architecture. This failure has resulted in inefficient fragmentation across the cashless industry worldwide.

NTT Docomo Disrupts the Mobile Payments Industry

Tired of waiting and being one of the leading pioneers globally, NTT Docomo formed a Japanese coalition by teaming up with Sony, which built specialized NFC chips called FeliCa for the Japanese coalition. Given the need for a financial institution across the payments value chain, it acquired a 34% stake in the Sumitomo Cards business.

It made another deal with Fujitsu to build FeliCa-compatible phones in 2005. By 2011, Fujitsu’s FeliCa-powered phones reached nearly 20% of NFC-enabled phones. Similarly, by 2015, NTT Docomo Osaifu-Keitai was used at more than 700,000 point-of-sales (POS) terminals across Japan. Similarly, over 37M Docomo subscribers have used Osaifu-Keitai payments services – making Docomo’s FeliCa-based payments service one of the few national successes worldwide.

The Device-Centric Secure Element Architecture

The device-centric secure element is a variant of the SIM-centric secure element. However, unlike the SIM-centric model, the secure element is embedded in the motherboard of the mobile handset. Unlike the SIM-centric model of the secure element, the device-centric model does not allow the chip removal or transfer to another device.

Another key departure from the SIM-centric secure element model is that the device-centric model gives more power to handset makers within the payment ecosystem. However, cooperation from MNOs may still be crucial in distributing the phones to their subscribers or users, which can be very disruptive.

The Host Card Emulation (HCE) Model

The HCE-centric secure element, launched in 2013, is a huge departure from either the SIM-centric and device-centric secure element architecture, given that the secure financial information is stored either in the cloud (remote location) or in a secure environment within a mobile phone but not in the SIM card or in the device itself. Android and Google Wallet use the HCE-centric model.

Like other secure element architectures, the HCE-centric model has some drawbacks. Unlike SIM card-powered secure elements, the HCE model does not work when the device’s power is off. An online connection is a necessity for making payments. Also, consumers need the latest NFC-powered Android to use the HCE-centric model.

Indeed, the fragmentation of the mobile payment ecosystem is axiomatic. As such, many strategic considerations are imperative to win in the cutthroat world of mobile wallets. Each strategy may increase or decrease the odds of success regarding how and when a payment company can reach the critical mass required to be among the industry leaders.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.