Threats From Dominant Digital Platforms: How can Firms Respond?

Credit card firms are in the business of smoothing out transactions between consumers and merchants at a fee. However, the sky-high costs of the leading and well-established firms, Amex, Mastercard, and Visa, invited competition in the mid-’80s.

Given this opportunity, Sears-backed Discover disrupted the industry by launching new credit cards that charged lower fees while offering superior credit balances. The firm used this pull strategy to attract more customers to its fledgling platform. As a result, many merchants began recommending the firm to its customers for its rock-bottom fees. As such, the aforementioned powerful competitors of Discover—the new entrant — reacted through contractual revision with merchants while inserting clauses (provisions) that discouraged this practice of suggesting their competitors’ cards to the consumers. Bitter lawsuits ensued.

By 2010, two well-established firms, Mastercard and Visa, moved on by settling the case. But Amex did not, given its history of charging merchants across its network sky-high fees. Moreover, it continued the court battle versus Ohio until June 2018. Indeed, the case demonstrates one of the most controversial elements in the platform (digital) model, which pits different antitrust perspectives against each other regarding the legality of such clauses (provisions) within their contractual agreements with merchants (sellers).

To be clear, the lawsuit against this $89 billion American payment platform is a different animal, given that the focus of the dispute was based on fees the platform charges and the rights of its network partners to limit other firms from advocating or suggesting other competitors’ card that charges rock-bottom fees to consumers.

Similarly, in February 2018, another MSP made the headlines. The Nikkei reported that Amazon Japan demanded financial contributions from vendors on its platform regarding its configuration enhancements. Again, two months later, on speculation that the $1.5 trillion e-commerce titan violated the competition laws, Japan’s Fair-Trade regulators did an incursion into its offices in Japan for investigation.

This is not surprising from a retail behemoth that owns an AI-powered medical records business. On top of this, it has a live streaming platform, an ad platform, a payment service, a leading book publisher, a fashion designer, and a forerunner in on-demand cloud computing through AWS, to name a few. It is clear that in most of these services, Amazon is among the vanguard of the industry’s bellwethers; this phenomenon has raised serious questions about its business model and, specifically, its anti-competitive practices while passing under the radar of regulatory scrutiny. For instance, the firm gleans valuable competitive insights regarding the vendors on its platform that it can use against them.

For this reason, we believe that the right time has come to update the global ill-suited competition laws. Most of the laws were crafted based on the realities of the heyday of industrial organizations—the pre-digital era. Just like the scholars who failed to grasp the inner workings of MSPs earlier, regulators woefully failed to grasp the implications of this emerging ecosystem business model on entrepreneurship, innovation, and democracy. Therefore, regulators need to take action as quickly as possible in the evolving business landscape.

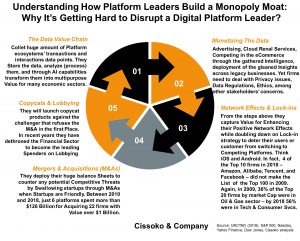

Recently, Facebook, in its quest to preempt any potential disruptor of its platform, went as far as to buy the Tel Aviv-based upstart Onavo in 2013, which provides the social media giant with powerful analytics capabilities. As such, it can monitor the performance of competitors and startups alike, which could be potential threats to Facebook’s business model. In addition, getting Onavo under Facebook Israel’s umbrella will enhance the firm’s preemptive capabilities regarding its rival platforms’ popular features. Indeed, against this backdrop of preemptive M&As, the number of 12-month-old startups has decreased by almost 50% in the United States alone in the past three decades. This drop is alarming.

So, the United States needs to get serious about antitrust law enforcement by increasing the number of positions at the U.S. Justice Department. Unfortunately, it is moving in the opposite direction, given that it is reducing them with the new Trump administration, which is cutting more than 130 staff at the Antitrust Division (ATR), including nearly 50 attorneys in 2018 alone. Unlike in the U.S., the EU’s antitrust regulators are assertive in acting against anti-competitive practices. That is why, in recent years, they have punished several tech behemoths regarding their suspicious behaviors, including their tax-dodging arrangements, such as those maneuvered by Apple with some European countries like Ireland.

Against this backdrop, the laws and regulations have teeth in Europe. In September 2017, through a very rude awakening, Uber was penalized by regulators in London with the revocation of its license to operate in the city regarding its non-compliant and often questionable behaviors. In addition, until December 2017, many MSPs were freeriding in that they were doing business in gray areas of the laws without clarifications regarding the industry these firms belonged to. They were doing business in many industries without being subject to their regulations. However, the verdict of the European superior court regarding Uber was a severe blow to the digital platforms (MSPs), as we know them, by ordaining that the disruptive ride-hailing firm is a transport business. This was a severe blow to the leading ride-hailing platform. Uber’s business model has been successful over the years and is based on non-market strategies centered on lobbying.

This may damage Uber and other similar platforms in the EU and worldwide. One of these platforms’ most significant competitive edges is the legal loophole that enabled them to scale faster than other legacy business models. The simple reason is that laws and regulations worldwide do not adapt fast enough to act on emerging business models. So, this gap has created a fertile ground for these network-effects-induced duopolies to strengthen their foothold.

Therefore, in the future, or if other jurisdictions follow suit, the business model of the ride-hailing services will suffer from the increased burden of costs and regulations, just like the legacy businesses, which will ultimately hinder their performance. This is not just a ride-hailing platform challenge but a ruling that should be a wake-up call for all platforms, especially Facebook and Twitter, which work like a typical media company using technology. The same goes for Airbnb, which crudely provides the same services as any other hotel but is not subject to several hotel regulations. Airbnb can be classified as a traditional hotel business at any time. As such, reclassifying these digital platforms as above will erase one of their key competitive advantages over legacy businesses, such as transport, media, and hotels.

By expanding the same logic, policymakers need to clarify whether mobile banking and payment applications are just digital platforms or financial institutions. Similarly, the same kind of question can be raised for healthcare-related applications enabling distance medical care, such as eHealth. Where do they belong? The implications and answers to these questions can tilt the playing field by adding more operating costs and elevating the entry barriers in these industries while reducing their attractiveness.

The New Generation of Disruption Judo From ‘Digital Platform Monopolists’

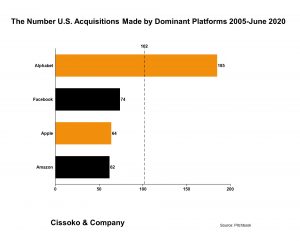

Unlike small- and medium-sized enterprises or startups, these behemoths have better resources than their smaller competitors. For one thing, they have the financial resources, massive data, data analytics, and artificial intelligence capabilities; they can afford the best talents that money can buy. With their eye-popping balance sheet, they can move quickly to crush any emerging potential competitor through mergers and acquisitions (M&A). For this reason, just six digital platforms—Facebook, Apple, Google, Facebook, Microsoft, and Alibaba – spent over $126. billion acquiring 22 potential rivals between 2010 and 2018—just on firms valued at $1 billion or more.

On top of these, over the decades, they have built lobbying power worldwide to twist the rules of the game in their favor, or at least to maintain them as they are. That’s why, in 2018, the tech sector—including the digital platforms—was the biggest spender on lobbying in the United States. However, despite all these capabilities, they fail to innovate at the speed of economic changes. As a result, many monopolist disruptors feel like cutting corners through an outright copycat rip-off is the only way forward.

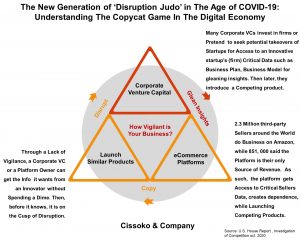

The two promising ways to access the inner workings of potential competitors’ businesses are through corporate venture capital, where a separately established venture capital of a giant corporation invests in a startup. In other instances, the corporate VCs pretend to be interested in buying a startup. In this scenario, when the startup’s management lacks vigilance or is too desperate to be sold out, it may reveal too much information to the false pretenders, allowing them to prepare their disruption launchpad and ultimately launch a competing product several months later.

The second option that the digital platform monopolists are deploying against the startups or SMEs is through their ownership and market power advantage as the leading digital platforms. Consider this: 2.3 million third-party merchants worldwide are listed on Amazon, while 851,000 said that nearly all their revenues come from the giant hybrid platform. They badly depend on Amazon while Amazon is milking their transactions and interaction data with customers of their target markets.

Given this advantage, Amazon employees have been reportedly leveraging third-party merchants’ data on its platform for launching disruptive private-label products against the same sellers, according to The Wall Street Journal. As a result of these unfair practices worldwide, including in Japan, the firm and other mega-platforms are on the cusp of antitrust disruption in the United States.

Amazon is not alone. Google and Apple have been abusing their unmatched dominance of Google Play and Store Apple’s App Store respectively for years by charging 30% on digital goods transactions. However, recently, many firms, including Netflix, Paytm, and Epic Games—the owner of Fortnite—said enough is enough. While Epic Games uses several means for disputes, Paytm has galvanized Indian companies to create an alternative to Google Play in India. The coalition is gaining momentum around the country. Recently, Spotify and Epic Games, among others, launched their nonprofit—the Coalition for App Fairness—to pressure the digital platform giants.

Many of these unfair practices and monopolistic behaviors will strengthen the antitrust cases against digital platform giants worldwide, particularly in the European Union and the United States, which are preparing for imminent legal action in the coming days. However, as we all know, many of these practices wouldn’t have been solved through legislation before then. Thus, organizations need to be vigilant to avoid being blindsided by disruption judo from leading digital platforms, including Alibaba.

In short, the digital economy is becoming increasingly complex, given the dominance of digital platforms within the world’s economy. Thriving entails a firm grasp of the inner workings of the platform world, knowing how to build organizational resilience, developing CEOs’ Strategy IQ for the challenges of COVID-19, and understanding how strategic thinking has evolved in the digital age.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.