Building Organizational Resilience: What do Winners Know That Others Don’t?

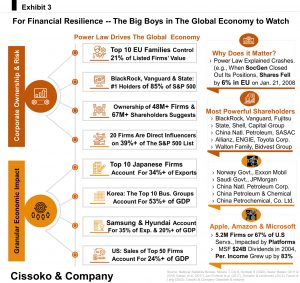

In a world where the top 10 wealthiest families control over 20% of the value of listed corporations in Western Europe, and three companies, BlackRock, Vanguard, and State Street, are the largest shareholders of more than 85% of firms listed on the S&P 500 (Exhibit 3), CEOs and business leaders need to rethink their strategies.

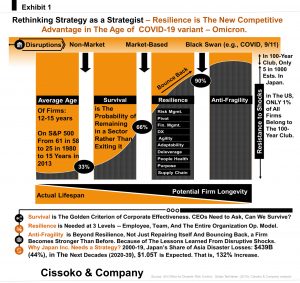

Indeed, beyond the competitors, companies need to double down on resilience – and craft strategies for longevity by becoming anti-fragile organizations. We are confronted with three types of disruptions in the 21st century. Market-based disruptions include supply chains, disruptive innovation, and competitors’ assaults. Non-market economic tensions include U.S.-China trade wars, Brexit, geopolitics, and public policies regarding climate change. Above all, the Black Swan disruptions, such as the 9/11 attacks, the 2008 financial crisis, and the COVID-19 crisis, are becoming more regular. On top of that, as climate change-induced natural disasters increase, Japanese companies need to double down on resilience strategies to mitigate $1 trillion in potential losses over the following decades.

As such, firms’ likelihood of being disrupted may come from these emerging and wicked disrupters rather than the usual competitive or market-based disrupters commonly assumed across industries. Thus, a fundamental rethink of strategy and the meaning of competition are becoming top priorities on the C-suite agenda. Worse still, most boardrooms lack expertise regarding many aspects of resilience, from cybersecurity to non-market disruption threats, which require boardroom and C-suite unity to tackle the immense challenges.

What do the Winning Companies Know That Others Don’t?

We believe that winning today means winning the resilience and anti-fragility battle. That is an organization’s ability to survive in, adapt to, and bounce back from expected and unexpected disruptions to its business operations.

However, our experience suggests that many business leaders and CEOs confuse resilience with adaptability and agility. They are not the same. Simply put, adaptability is the re-establishment of fit with the environment, and in many cases, it is focused on the external environment. As such, while adaptability is a core element of resilience, adaptability alone doesn’t mean resilience. Given that many adaptable organizations do not display some crucial aspects of resilience, learning from shocks and bouncing back to the pre-crisis level of performance.

Similarly, some organizations are confusing agile or agile at scale with resilience. Again, agility in all its forms is one of the key building blocks of resilience. However, the ability to be nimble and make a swift move does not guarantee resilience. A team needs more than an agile way of working to be considered resilient. The first litmus test of team resilience is the trifecta of communication, compromise, and coordination in times of disruption while bouncing back to the pre-crisis level of disruptions.

In other words, can the team bounce back after losing a teammate, a product development failure, or losing a top account? If the answer to any of these questions is no, for example, you have failed the transition test from an agile team to a resilient one. Thus, the team should be considered to be just an agile team. Similarly, a team can’t be resilient if it can’t minimize and manage risks proactively by doing whatever is necessary to reach the finish line through persistence and grit.

Beyond adaptability and agility, resilience calls for robustness, redundancy, resourcefulness, rapidity, and change capabilities. A litmus test of resilience in the age of unprecedented disruptions is the ability to improvise the capability of responding with few resources at a firm’s disposal without advanced planning. Failure to do so means a deficit of resilience capabilities within an organization.

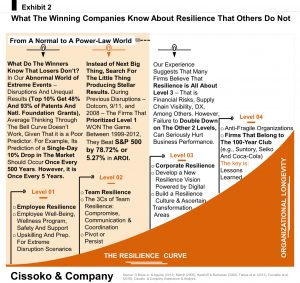

Above the defensive mechanism to build resilience, the pre-emptive strategy that winning companies know is the mastery of the performance game across the modern economy. Instead of wasting time and resources searching for the next big thing, the winning firms search for and do the little things that boost the corporate performance on steroids. For example, there are four layers of resilience in building resilience. Beginning with employee resilience, followed by team resilience and corporate resilience. Within the realm of corporate resilience, we have degrees of resilience.

The minimum requirement of corporate resilience calls for the following steps:

- Developing a new vision of resilience powered by digital.

- Understand the triggers for doubling down on resilience (Exhibit 1).

- Build a digital culture.

- Establish a digital organization.

- Ascertain the transformation areas needing resilience.

- Evaluate impact.

In this resilience game, it needs to be clear that building organizational resilience is a nonstop endeavor that needs to be institutionalized. Again, what do winning firms know that others don’t? A resilient corporation does not necessarily mean it has resilient teams or resilient employees. Similarly, having resilient employees within teams does not necessarily make the teams resilient. Further, having resilient teams within the organization does not necessarily make the entire corporation resilient.

Above all, the ultimate level of resilience is anti-fragility—where a company becomes so strong that it builds muscles of organizational longevity to join the 100-year club, such as Suntory, Seiko, and Coca-Cola—which results from the lessons learned from previous shocks throughout a firm’s lifespan.

Rethinking Individual and Corporate Performance and Financial Risks

The devastating disruptions of COVID-19 have demonstrated that organizations and their CEOs are more interested in the implications of extreme events than the averages. Given its vanishing tails, the normal distribution allows the analysis to be focused on limited variance and stable means in the data. As such, the normal distribution is a poor predictor of extreme events disrupting the world economy. For example, a single-day 10% market drop is predicted to occur once every 500 years. However, it happens every five years.

Again, when it comes to improving corporate performance through resilience, the level of resilience that had the biggest impact on performance during other previous disruptions, such as dotcom, the 9/11 attacks, and the 2008 financial crisis, is employee resilience, which is often the most neglected part of the resilience equation.

Organizations that doubled down on this level of resilience saw their shares beat the S&P 500 by more than 78% over 13 years. Again, this is another testament that the power-law distribution increasingly shapes performance—not the normal distribution—in the modern economy (Exhibit 2).

With the dominance of the normal distribution in scientific research, such as intellectual quotient, stock market analysis, and economic trends forecast, it has been assumed without question that individual performance is normally distributed.

However, according to our experience, consistent with the findings of O’Boyle Jr. and his colleague, individual performance follows a Paretian distribution. Indeed, they analyzed nearly 200 samples and individual performance data of 630,000+ across various industries and job functions. The data includes the performance of politicians, athletes, professional players, amateurs, and academic researchers. The findings suggest that individual performance conforms to the Paretian distribution, not the Gaussian distribution — as previously assumed by organizations and advisers. That’s why, in recent years, many organizations, from GE to Microsoft, have abandoned the flawed practices of stack ranking employees because they have realized that it doesn’t work as previously thought.

This analysis revealed that the power-law effects are observable everywhere – from individual to corporate performance. Consider this: in South Korea, the 10 top business groups account for nearly 55% of the GDP and 50% of exports, while the leading company, Samsung, accounts for almost 25% of exports and 15% of South Korea’s GDP. Moreover, the impact of Samsung and Hyundai is deep as well. They account for nearly 35% of exports and over 20% of Korea’s GDP. Similarly, Japan’s top 10 companies, including Toyota and Itochu, account for over 33% of Japan’s exports. In the United States, a similar Paretian image emerges; the revenues of the top 50 companies represent nearly 25% of the country’s GDP.

Why does it matter? Consider this: over the 15 years through 1999, during Japan’s bubble economy, the growth average standard deviation of the top 25 firms was around 8%, while the median was around 20%. Similarly, at the end of December 2004, a one-time $24B dividend payment that Microsoft made boosted the American personal income growth by 83% (from 0.6% to 3.7%), according to the U.S. Bureau of Economic Analysis (BEA) findings in 2005. Furthermore, during the rogue trade scandal at Societe General, it closed out its positions, which resulted in a 6% European stock market fall on January 21, 2008. As a result, the U.S. Federal Reserve had no choice but to cut interest by 0.75%.

The triple whammy of Black Swan disruptions, non-market and market-based disruptions are here to stay. The winners will be the companies that have learned lessons through their own experience, the disrupted firms, and the anti-fragile organizations. Thus, in the age of disruptions, competitive advantage will be based on building resilience by knowing that the normal distribution view of averages doesn’t work. We are indeed in a world driven by the power-law distribution of performance, disasters, and economic shocks.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.