Rethinking the ¥700Billion Money Problem of Japan’s Finance and Insurance Industry

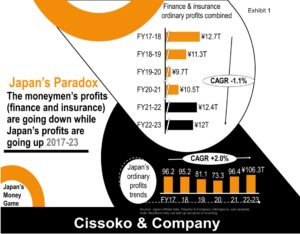

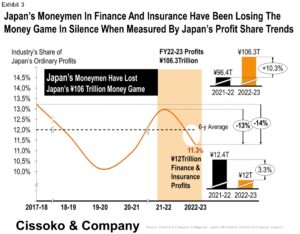

Our analysis revealed that Japan’s moneymen have silently lost the money game across the financial industry when measured by their share of Japan’s ordinary profits over the years. Profit share recovery—let alone winning the money game—will require bold strategies regarding the financial industry’s money-making formulas in the coming years. Otherwise, their ordinary profit share will drop below the psychological threshold of 10% share. For one thing, at the end of the fiscal year 2022-23, shares stood at 11.3%. Shares are now 21% below the previous year (the fiscal year 2021-22), 10% below the industry’s six-year ordinary profit share average, and 15% below the fiscal year 2017-18— a perfect downturn trifecta.

Corporate Japan’s Profitability Remains Resilient across all Sectors, but the Moneymen

Worldwide, the COVID-19 outbreak was disruptive, to say the least. And the Land of the Rising Sun is no different. Indeed, in the two years preceding the outbreak, corporate Japan made an average of ¥88 trillion. However, the ensuing disruptions knocked Japanese businesses’ total ordinary profits to nearly ¥70 trillion.

A second-order effect of the COVID-19 outbreak was sending global supply chains into a tailspin. Despite all these formidable business challenges, given the hard-learned resilience lessons from past disasters, Japanese companies’ profitability improved through the fiscal year 2022-23. In other words, corporations managed to hit a 2% compounded growth rate over the five fiscal years, which ended on March 31, 2023.

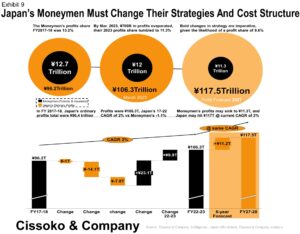

Moreover, profitability jumped 10% year-on-year to hit the ¥106 trillion milestone, which is a clear testament to the fact that in Land of the Rising, the profitability sun is still rising. Thanks in part to the depreciated Japanese currency, we believe that CEOs need to double down on their commitment to the Japanese market like Warren Buffett by winning what we call “Japan’s ¥106 trillion money game” before the party is over, given that no window of opportunity remains open forever. The exception to this trending profit boost was Japan’s financial industry, which saw its profits sinking in the opposite direction by 3%.

Japan’s Moneymen Have Lost Japan’s Money Game – the Profit Game

Over the past six years through March 31, 2023, corporate Japan’s profits grew at a 2% compounded annual growth rate (CAGR) versus a -1.4% combined loss for the moneymen in the finance and insurance industries. Moreover, in the fiscal year 2022-23, the total ordinary profits of Japanese firms soared by 10% against the previous fiscal year compared to -3.3 % for the moneymen—the combined ordinary profits of the finance and insurance industries.

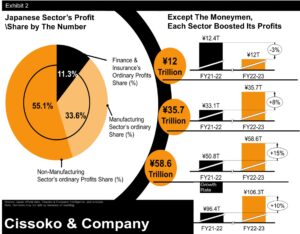

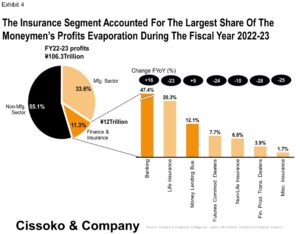

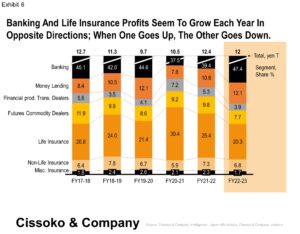

Furthermore, our analysis revealed that Japan’s manufacturing sector improved its profit pool by 5.8%, and the non-manufacturing sector, excluding the finance and insurance industry, boosted its profit pool by 15% against the preceding fiscal year. However, the financial industry (banking, money lending business, futures commodity transactions dealers, and life and non-life insurance institutions, among others), within the non-manufacturing sector, was among the industries that saw more than a 3% decrease in their previous profit pool share of ¥12.4 trillion.

Japan Insurance Industry has Been hit Hard by Profits Erosion

Specifically, Japan’s banking industry—with its 47% share of the ¥12 trillion ordinary profits made during the fiscal year 2022-23 by the combined financial sector—saw its profits increase by 16% to ¥5.7 trillion. Similarly, money lending firms improved their previous fiscal year profits by 10% to hit ¥1.4 trillion by joining banking to become the two resilient segments of Japan’s financial industry.

However, the life insurance industry lost 23% of its previous ordinary profits, decreasing to ¥2.4 trillion in fiscal year 2022-23. In other words, the insurance industry accounted for the majority (33%) of Japan’s financial industry profit loss during the period, including the 10% profit loss from non-life insurance.

Profit Size and Growth Trends Across Segments

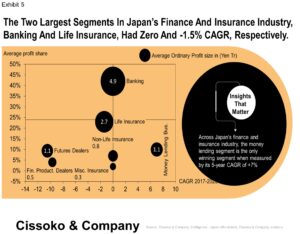

Our analysis revealed that profitability performance across the seven segments has been abysmal, and spectacularly so, given that three among the seven segments had zero compounded growth rate from 2017 to March 2023, while the other three segments, life insurance, futures dealers, and financial product transaction dealers, had the worst performance.

Only the money lending business segment produced a 7% compounded growth rate (CAGR) during this period. The banking segment did better than all segments by boosting its profits against the previous fiscal year by 16% through resilience and reached its 2017 profitability level of nearly 5.7 trillion. However, we can’t call this bounce-back winning. The lesson for CEOs across financial institutions and beyond is that being profitable and winning the money game when measured by profit share trends are two different things.

To better understand the Japanese finance and insurance industry’s competitive landscape, we analyzed the segments on three dimensions: average profit share, average profit size, and each segment’s compounded growth rate between 2017 and 2023. Through this lens, it becomes clear that the money lending business is emerging as the most promising segment for the moneymen despite its small profit size compared to banking and life insurance.

Scenarios from Recovering Back Profit Share Lost to Winning the Money Game

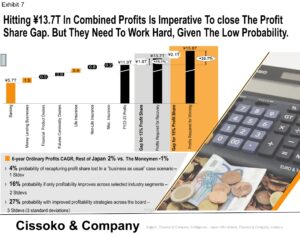

Our analysis suggests that the moneymen will need to hit between ¥13.2 and ¥15.9 trillion, respectively, for-profit share recovery and to return to the winning track. For one thing, the moneymen have lost nearly 15% of Japan’s profit share in just six years, based on the opposite trajectories of their industry (finance and insurance) compounded annual profit growth rate (-1%) and Japan’s as a whole (2%). This silent disruption went unnoticed by many CEOs and business leaders. It will make the profit share recovery – let alone win again by acquiring profit share above the fiscal year 2017-18 level—very challenging. However, it is possible, assuming Japan’s profits remain at their current (FY22-23) ¥106 trillion or above.

Indeed, this recovery will depend on the future economic environment and Japan’s moneymen’s ability to enhance their profit-making formulas. At a minimum, their combined profits in the finance and insurance industry need to top ¥13.2 trillion. And to declare victory, they may need to hit ¥15.9 trillion in combined ordinary profits. As such, under varying scenarios, they can recover sooner than later due to the improvement in their strategies—the profit-making formulas.

These probabilities are 4% for the current business as usual, 16% regarding strategy improvements across the key industry segments, such as banking and life insurance, and 27% when all players adopt serious profitability enhancement strategies.

The Difference Between Being Profitable and Winning the Money Game of Japan’s Finance

Our experience suggests that cognitive dissonance is troubling the business management and economics world, given that we tend to gauge most variables as a percentage of GDP, such as tax-to-GDP ratio or defense spending to a country’s GDP. Similarly, for growth, market share takes center stage; each firm strives to gauge its market share at an industry level. However, when it comes to corporate profits (including industries’ profits), companies turn to accounting and financial metrics such as return on equity and total shareholder return (TSR), given the rampant short-termism and mounting pressure from financial analysts.

However, when it comes to corporate profits (including industries’ profits), companies turn to accounting and financial metrics such as return on equity and total shareholder return (TSR), given the rampant short-termism and mounting pressure from financial analysts.

Industries’ profit share at the national level, including their strategic implications, rarely matters. Moreover, flawed assumptions exist, given that most CEOs and business leaders are used to reading Japan’s GDP growth rates and other economic indicators but rarely—if at all—think about a country’s profit growth trends. That’s one of the reasons the financiers may have believed that Japan’s finance and insurance industry’s profit growth rates are equal to Japan’s total profit growth rates—because there is no divergence or difference between the two profit growth rates. This conventional mental model may have blindsided Japan’s finance and insurance industry’s business leaders. As such, most people across the financial sector—if not all—are surprised by the impersonal insights in this report, which investigated the industry’s future through a different approach using ordinary profits.

Simply, firms compete for their industry’s profit share while industries compete for more national (including global) profit share. When an industry’s profit size shrinks, competition increases while attractiveness decreases simultaneously. And incumbents may find it hard to grow organically, which may pressure the leaders to embark on rushed and misguided financial engineering, such as mergers and acquisitions (M&As), to enhance their prospects by hoping for elusive synergy.

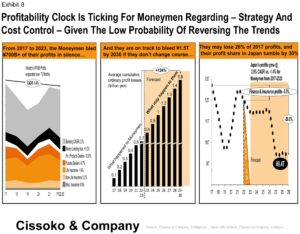

Indeed, the clock is ticking for Japan’s finance and insurance moneymen to quickly craft strategies to boost their profitability while controlling costs at scale. The problem in the industry and beyond is that most companies are used to the traditional financial performance key performance indicators (KPIs) such as total shareholder return (TSR), return on equity (ROE), return on assets (ROA), etc. While still relevant for comparing performance across industries, these KPIs have serious flaws, given that they may distract business leaders in ascertaining the firm or its industry’s profit share trends and making the required bold strategic moves.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.