GenAI Pitfalls Lessons From Japan: Why Productivity Does not Mean Profitability

The potential of artificial intelligence has been a topic of discussion for decades. The emergence of large language models (LLMs) that power ChatGPT and Gemini, among others, has brought this potential to life. These technologies have disrupted the economic landscape, offering new levels of productivity and capability. It’s no wonder that companies across all industries—large and small—are eager to adopt these technologies, driven by the promise of game-changing potential.

As such, like FinTech innovations before GenAI, many resources will be wasted in this quest for an elixir to boost corporate performance, considering stratospheric costs associated with the large language models, including their negative impacts on climate change. While the productivity potential of these innovations has been hyped, missing from the C-Suites and boardroom discussions is that productivity does not necessarily mean profitability. Simply put, firms in their GenAI gold rush must not lose focus on the 3Ps of profitability. Failure to do so will lead to the obvious: poor corporate performance due to the failure to discern between value creation and value capture. To illustrate this productivity pitfall, we must learn from Japanese pharmaceutical firms in the 1980s.

Behind The Gold Rush: Tech Firms Dominate the Global Economy

The economic profit of Japanese technology firms has jumped by 127% in 10 years—from nearly $11 billion in 2013 to $25 billion in 2022. This means the median economic profit per firm soared from $2 million to $3.6 million over the same period. Moreover, the number of firms soared from 483 to 564.

According to Goldman Sachs, the so-called magnificent seven accounted for nearly a third of S&P firms’ valuation in 2023. Moreover, when it comes to economic profit (EP), their influence can be felt across all listed firms in the United States, given that the seven firms accounted for more than a third of the economic profit.

Cloud Computing, GenAI Startups, and Chipmakers Partnerships

In this new competitive landscape, no firm can go it alone. Adaptability related to cloud infrastructure regarding the fast-evolving generative AI player’s latest models and computing imperatives has posed serious challenges to the three cloud kings: Amazon (AWS), Microsoft Azure, and Google Cloud. Similarly, hardware and chipmakers such as Nvidia need to move at GenAI’s speed of demand regarding GPUs. In this emerging world of disruptive technologies, strategic alliances, including innovation (R&D) partnerships, have become the new game in town.

Two kinds of partnerships have emerged. The Microsoft-OpenAI partnership is exclusive, while other partnerships formed by Amazon Web Services (AWS) with Hugging Face (2023) and with Anthropic (2023). Similarly, the partnership formed by Google Cloud and Cohere (2021) and the one formed by Google Cloud with Anthropic in 2023 are all non-exclusive partnerships. In other words, while the big technology firms have firepower regarding infrastructure as a service (IaaS), platform as a service (PaaS), and software as a service (SaaS), including chipmaking prowess, the startups, particularly OpenAI are the leaders of GenAI large language models (LLMs).

Beyond the LLM models (BERT & Claude, for example), winning requires computing infrastructure in the cloud and advanced chips for data processing, including large memory. This emerging ecosystem thus brought together cloud giants like Amazon Web Services (AWS), Microsoft, and Google, semiconductor powerhouses such as Nvidia, TSMC, and Samsung, among others, and large language model (LLMs) leaders like ChatGPT. Indeed, the digital and technology ecosystems are getting deeper by the day because players have no choice but to partner with like-minded allies.

Japan’s Operational Excellence Productivity

Japan is well known as the paragon of operational excellence and the birthplace of many of the management frameworks taught at leading MBA programs worldwide, including Just in Time (JIT), Kanban, and Total Quality Management (TQM), among others. Indeed, Japanese corporations were among the best students of Edward Deming’s statistical quality control. Combining these productivity and efficiency techniques (including state interventions) enhanced Japan’s productivity and propelled the country to the world’s second-largest economy in the 1970s—the Japanese miracle years. Like in many global industries, such as electronics and cars, the Japanese pharmaceutical industry was no exception.

Why Productivity Does Not Necessarily Mean Profitability

The pharmaceutical industry, like high-tech, is capital-intensive and innovation-driven. Huge R&D innovation investments are required each year to be at the top of the game and succeed. With many innovation KPIs to track, many firms are distracted and sometimes confuse productivity and profitability, which are two different things.

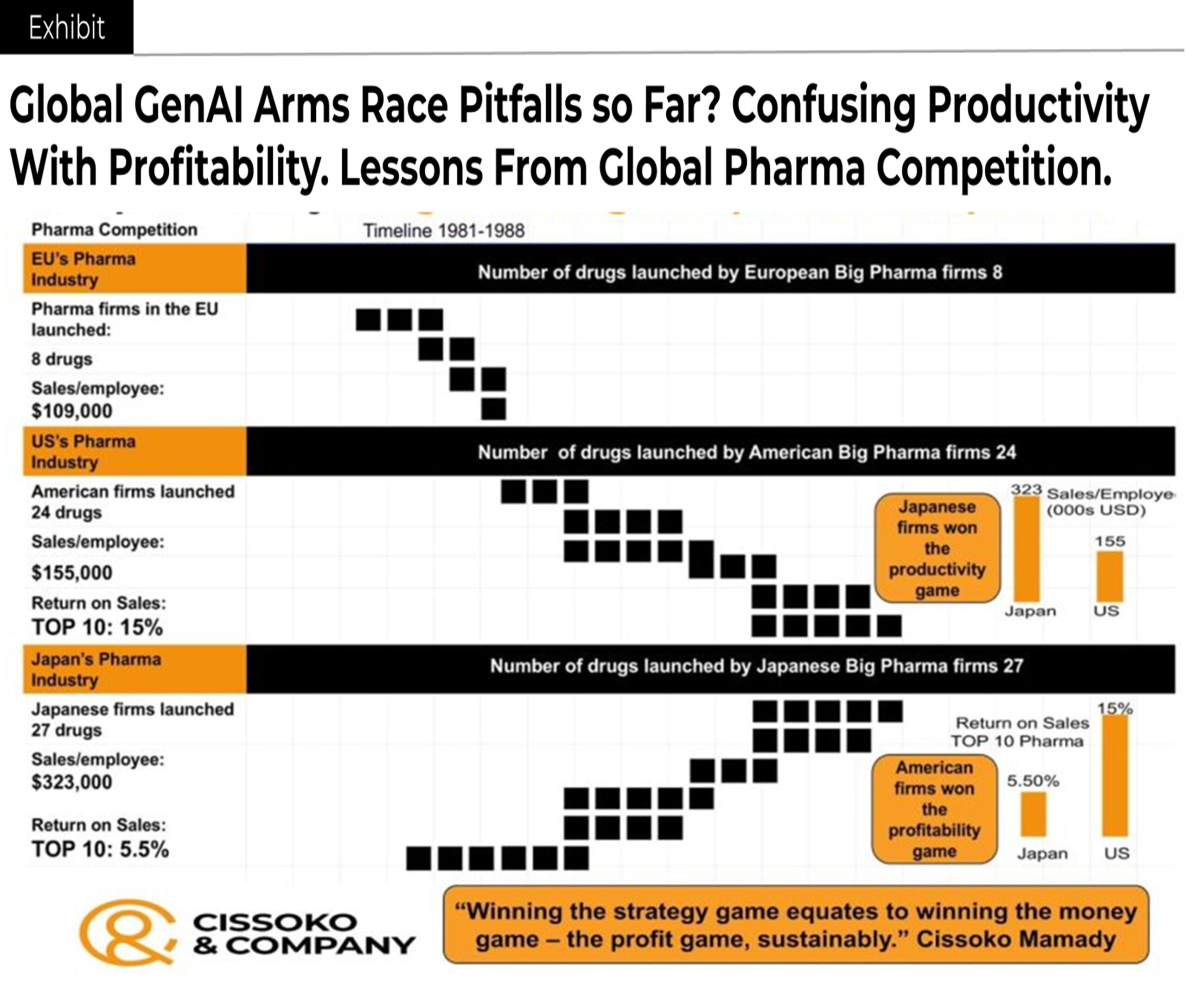

Between 1981 and 1988, European pharma companies launched fewer than eight drugs with productivity of $109,000 as measured by sales per employee. The American pharma firms launched 24 drugs using the same productivity yardstick; their sales per employee stood at $155,000, and the return on sales (ROS) of the top 15 companies was 15%. Regarding the Japanese top 10 pharmaceutical firms, by contrast, they were more productive than their American competitors, with $323,000 in sales per employee. However, the Japanese pharma giants lagged behind their American rivals in terms of profitability. Indeed, the Japanese biopharma companies’ return on sales (ROS) was nearly 60% below their American competitors—a 5.5% return on sales (ROS) for the Japanese versus 15% for US biopharma giants. This analysis revealed that while CEOs and business leaders talk a lot about corporate productivity, many fail to realize that high productivity does not necessarily mean high profitability.

In this age of GenAI Gold Rush, Don’t Lose Sight on the 3Ps of Profitability

Our decade of experience suggests that winning the game of strategy means Winning the Money® Game™ sustainably. Indeed, profitability reigns supreme among the variables highly correlated with stock prices and total shareholder return (TSR). Furthermore, launching disruptive innovations or being at the forefront of GenAI must not be an excuse for losing focus on key financial performance metrics. For one thing, sooner or later, investors will ask the fundamental question: What are we gaining from all these innovations and investments in GenAI? What are the returns from all these innovations? Why is the firm taking so long to boost profitability? These are valid questions that CEOs and other business leaders need to consider regarding strategy, innovation, and business models in this age of war and high interest rates.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.