Building COVID-19 Resilience Through Pivot: Capitalize on $700 billion Opportunities

The economic and disruptive impacts of the coronavirus pandemic are axiomatic. Every day, there is more bad news regarding the economy, the rise of COVID-19 cases, and its death toll, which have resulted in serious anger in the UK recently. Because it has been found that over 40% of deaths in Wales and England are in care homes, on the other side of the Atlantic—in the United States—depressing economic figures have been reported throughout the week. For example, just this week, the number of people filing for unemployment claims topped a cumulative 36 million in the U.S. alone. To put these figures into perspective, this number is nearly the entire population of Florida and Massachusetts combined.

Similarly, retail sales in the country were shocking. According to The Wall Street Journal, they plunged by more than 16% in April, while the clothing sales went down even further by tanking more than 85% because of the apparent consequences of the stay-at-home orders. The jaw-dropping report continues with a nearly 13% and 30% fall in groceries and restaurant sales, respectively. Moreover, electronic sales fell by almost 61%, while manufacturing shrank by nearly 14%—a record contraction in recent history. To be sure, any crisis has a silver lining.

For one thing, the demand for COVID-19-related products is on the rise across the globe, while other sectors are shrinking at an alarming rate. We believe that organizations need to capitalize on these opportunities to build resilience.

Furthermore, since early autumn, the second wave of COVID-19 began to raise its ugly head across Europe and many parts of the world, including Israel. We anticipate new restrictions to send the world’s economy into another tailspin. Again, according to our research, we anticipate vaccines from summer 2021 at the earliest.

Moreover, another challenge that businesses need to consider is the efficacy of the vaccines. In other words, vaccines come in varied forms regarding efficacy. Thus, the question is: how effective will the vaccines be, 30%, 50%, or 65%? Another issue exacerbating the challenges is that a huge percentage of the population is allergic to vaccines within many countries around the world—meaning they do not want and dislike vaccines.

After overcoming these hurdles, we need to deal with the logistics challenges regarding the distribution of vaccines worldwide. It will take over 7,900 commercial planes—nearly 30% of the entire global commercial fleet in 2020, which is a serious challenge by any measure. On top of that, many planes may need adaptation to carry the vaccines between 2°C and 8°C globally. Indeed, it may take up to 2025 for the entire global population to be vaccinated. Thus, strategic foresight will entail a pivot across many industries to thrive or at least survive the Black Swan disruptions of COVID-19. Experience suggests that organizations that follow one of the seven types of pivots have a greater likelihood of survival during times of economic storms.

The Coronavirus Crisis New Game in Town: Pivot Through Organizational Agility

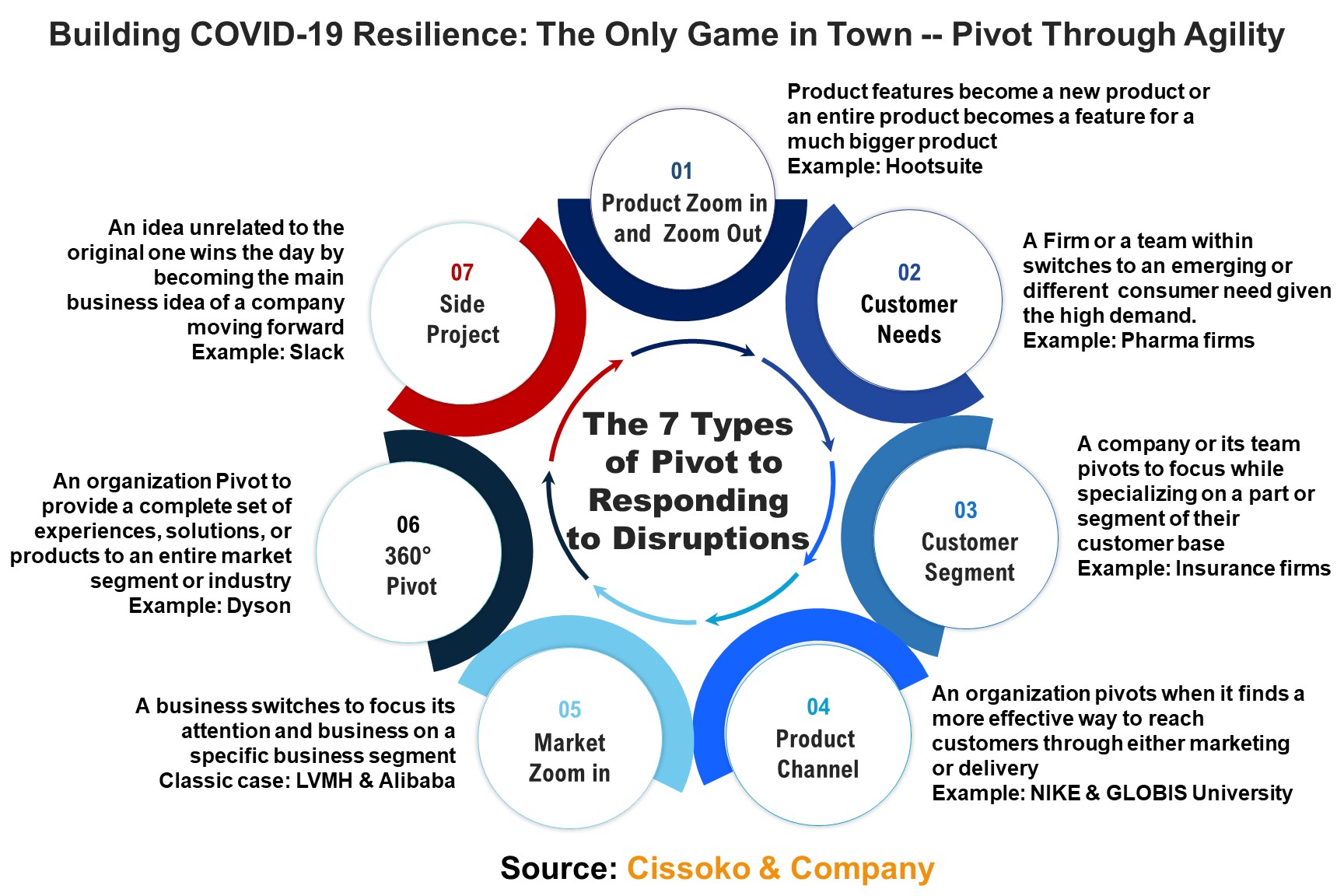

With just one vaccine candidate in a phase 2 trial, four in a phase 1 trial, and nearly 55 in preclinical studies, the best hope for the availability of either one will be in the fall of 2020. Thus, we believe that organizations cannot afford to wait until that time to resume business, which may be a dangerous gamble even for the most resourceful firms out there. The least resourceful with already tiny margins may go bankrupt by then. Thus, we believe that pivoting through organizational agility is a valid playbook for building resilience against COVID-19. Indeed, a pivot is not just the purview of the startups in Silicon Valley but also the large organizations and their dormant capabilities and capacity. This article will guide pivoting organizations in this age of Black Swan disruptions. In our experience, there are seven types of pivots for responding to disruptions:

Side Project—an organization pivots by double downing on an idea unrelated to the original. As a result, this unrelated idea becomes the driving force to change the game. The classic case is Slack, initially trying to build an online game termed Game Never-ending. Unfortunately, the business went sour. Also, the founder, Simon Butterfield, tried again to make another one, which he called Glitch. Again, that one, too, was a failure. During these startup projects, he developed a remote communication tool for collaborating with international colleagues, which is now the famous Slack that most of us use daily—now valued at over $5 billion.

Product zoom in and zoom out—based on the traditional concept of incremental innovation. It entails an improvement of one product feature through adaptation. This can be decoupling combined features as a standalone product or recoupling features (combination) of different products as a new product in another way. For example, many marketing software firms, such as Hootsuite, have used this product adaptation strategy to serve many social media customers through a single software or platform. Before this kind of pivot, people interacted with most social media apps individually, which was time-consuming for busy people.

Emerging consumer needs—In this pivot case, an organization switches gears by focusing on an in-demand consumer need that it has the capabilities or capacity to serve better. This type of pivot will focus on this article, given the rising need for COVID-19-related products that many organizations can capitalize on because of the shifting consumer needs and wants during this pandemic. In contrast, many factories are idle or running at low capacity.

Pivoting by specialization on a specific segment or part of the market—this pivot strategy helps an organization direct its corporate energy and resources by avoiding a losing game of casting a wider net in a competitive industry or a sophisticated market, demanding more expertise and resources. For example, competition within professional service firms can be brutal, while clients want more expertise across fast-changing industries. Thus, what smaller consulting firms do in this kind of environment is to build a reputation in a specific niche.

Product or service channel pivot—organizations need to explore most if not all, types of marketing channels when delivering products or services. For example, many academic institutions have been hit very hard by the coronavirus crisis. Given that, regarding their decade-old reputation, they refuse to consider the online channel as a great delivery option even with all the technology available right now.

GLOBIS University Graduate School of Management in Tokyo already provides an online MBA program option. When the coronavirus disaster struck, Japan’s number one business school doubled down on its online program within a few days. This channel pivot has been a great success story among business schools in Japan. Similarly, after closing its offline channels because of the lockdown orders, Nike could thrive in many parts of the world through its online channels. Many brick-and-mortar retail megastores have been seriously disrupted, as mentioned above, because of the deficit of e-commerce options and other digital-enabled delivery channels. That’s why the direct-to-consumer (D2C) model—such as Unilever-acquired Dollar Shave Club—took many traditional retailers off guard when the disruptor provided products through digital technologies bypassing the traditional middlemen in the sector, such as Target.

Thus, we anticipate that many will double down on their digital transformation in the coming weeks. For one thing, the status quo is no longer an option. Furthermore, the retail banking sector, too, with its complacency-induced blindness and its over-reliance on ATMs across many countries, has been seriously upended by the stay-at-home orders—given that more than 1.6 billion people around the world were under lockdowns—at the height of the pandemic. That’s why in the nine years through 2019, over 11,000 full-service bank branches have closed in the United States alone. While traditional retail banking is closing its doors, Alibaba’s Ant Financial Services Group business is booming, given the tailwind from the lockdowns across China. For this reason, many banks are desperately hunting for their digital technology arsenal to build mobile applications. As a result, the firm’s clients jumped by more than 170% in the eight weeks through April. It became the envy of the industry within just a short period.

Market zooming—this is similar to the above pivot. However, the key difference is that instead of pivoting by focusing its attention on specific products, the firm doubles down on a specific market by deploying its full capabilities in that direction. Most firms adopt this strategy for business expansion, intense industry competition, counter-attacking new entrants, and other strategic considerations. This is the strategy that some call growth through granularity. Because within an industry, not all segments perform equally in a given state of the economy or disruptions. Thus, vigilant organizations pay more attention to this market intelligence for pivot opportunities. To be sure, the window of opportunity for pivoting varies by sector.

Speed and organizational agility are crucial for capitalizing on these emerging opportunities. The classic examples are Louis Vuitton Moet Hennessy (LVMH) and Dyson. Given the dire shortage around the world, LVMH pivoted its perfume lines to the sanitizer market. This move helps the firm align its strategy with its purpose by doing well and doing good. In the case of Dyson, it made a prototype for ventilators within a few days and got 10,000 orders from the British government. Unfortunately, it was reported later that the orders were no longer needed. Furthermore, the Japanese fashion giant Uniqlo volunteered to make millions of face masks and ship them worldwide in places where the shortage meant death warrants.

Before the COVID-19 crisis in the 80s, Toyota dedicated considerable capabilities to compete in the luxury segment of the automobile sector by launching Lexus—one of the world’s top brands. The firm knew its reputation for making high-quality cars at a reasonable price was no longer good enough, given the rising competition from other Japanese rivals. Thus, the firm decided it was time to move to the profitable luxury segment to enhance its market share while broadening its customer segment by appealing to social status-conscious customers. The result of the pivot was beyond Toyota’s wildest dream.

The 360° pivot—the most challenging of all. It calls for a complete transformation through real strategic reorganization. Because the organization needs to pivot in products and segments or products and industries simultaneously, it demands a great deal of strategic and organizational ambidexterity. When it succeeds, it can be a great leap forward. However, when it fails, it can jeopardize an organization’s future viability while seeding doubt within. For example—Dyson—the British vacuum cleaner powerhouse, tried this kind of pivot by moving into the self-driving car industry given the hype a few years ago. The firm spent billions of dollars by moving to Singapore. However, a few years later, the project was abruptly aborted.

Challenging as that may seem, correctly done, it can be the best strategic move an organization can undertake. This kind of pivot, unlike the others, requires visionary leadership, change management, and, above all, building a new culture for a new direction. IBM’s pivot is one of the most successful 360° pivots in recent memory. It was so successful that its former CEO, Louis V. Gerstner Jr., wrote a best-selling book titled “Who Said Elephant Can’t Dance.” He revealed that the success of his turnaround efforts was based on shaking up the culture of the behemoth IBM – by reorienting the firm from its hardware root to its services. Thus, he said that organizational culture is not one of the most important elements of an organization—but the most important element for its success. Building a healthy organizational culture was the secret behind the successful transformation of Microsoft by its CEO, Satya Nadella. The move made Microsoft more relevant to the digital economy when he doubled down on cloud computing and strategic acquisition of the professional platform giant LinkedIn.

The Game in Town—Capitalizing on the COVID-19 $700 Billion Pivot Opportunities

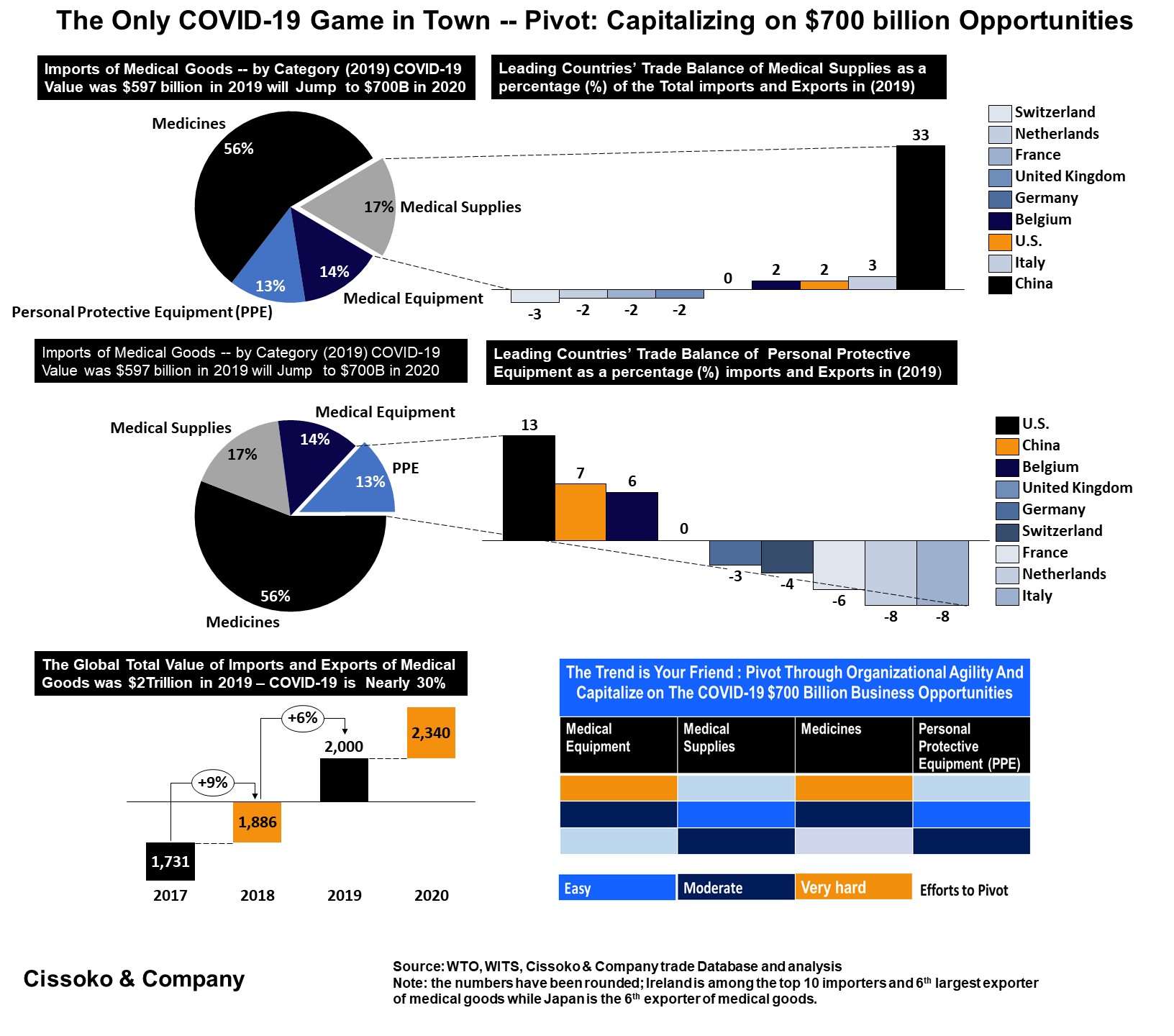

Demand is waning across industrial sectors such as Fast fashion, with over $140 billion, tourism, durable goods, and automotive at stake. Yet the COVID-19-related products are in demand, including:

- Personal protective equipment – face masks, hand soap and sanitizer, protective spectacles.

- Medical equipment technologies – telehealth and health tech

- Medical supplies – used for hospital consumption, including alcohol, syringes, gauges, and reagents.

- Medicines – pharmaceutical products such as bulk medicines

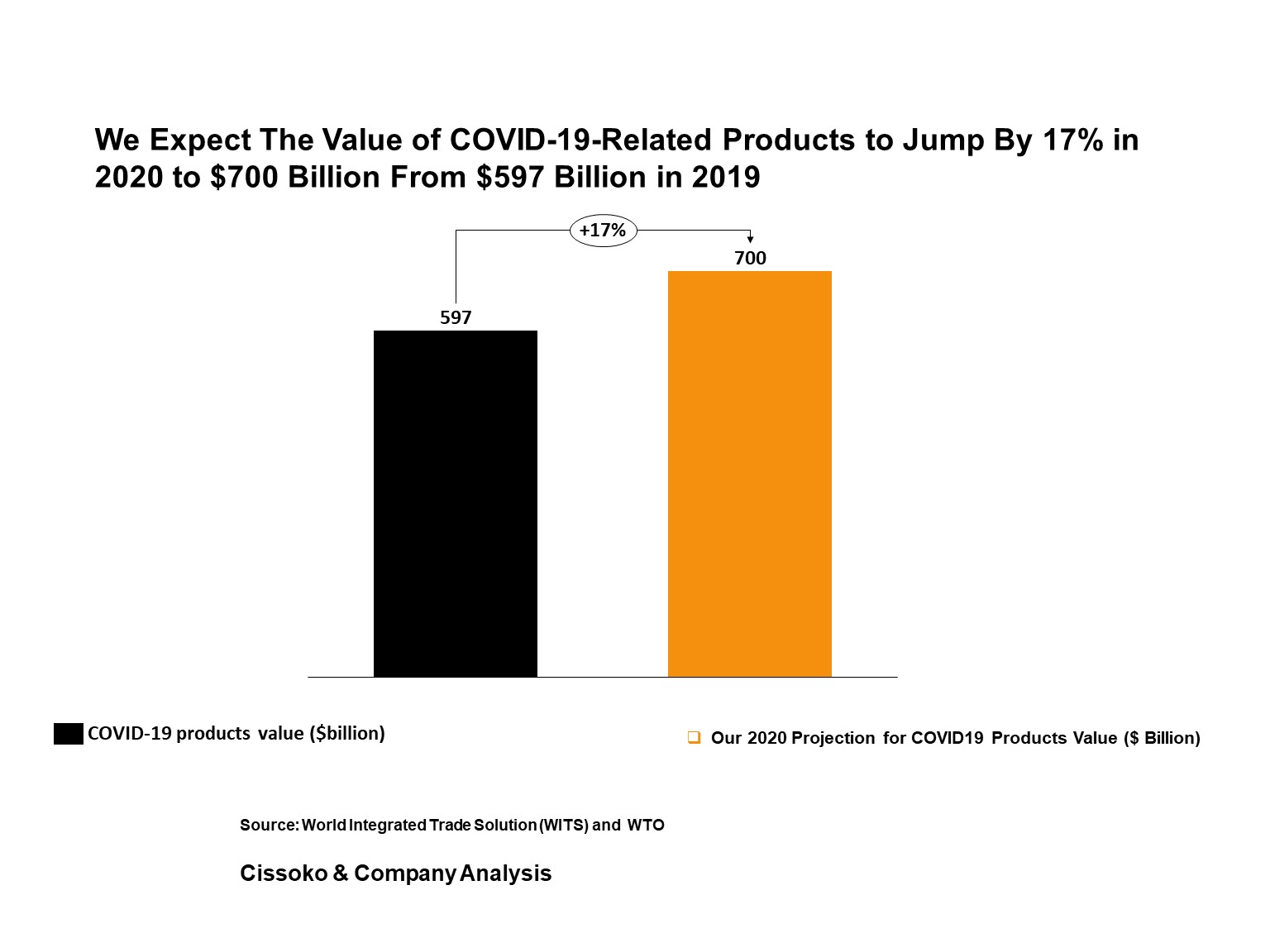

The market for these products is booming, given the coronavirus crisis. The value of these products in the market was nearly $600 billion in 2019. We anticipate it will reach a whopping $700 billion in 2020—equivalent to almost 30% of the total value of the global medical products imports and exports in 2019, which was $2 trillion. Organizations need to be vigilant in this time of volatility, uncertainty, complexity, and ambiguity (VUCA). Indeed, our research suggests that the global value chains (GVCs) will be gradually regionalized and nationalized for national security reasons, and the coronavirus crisis has been laid bare.

Pressures will increase on many firms in critical sectors of economies—in developed and developing — to make a U-turn through coercive pressures and subsidies. The good news is that the average tariff applied to these medical products in most countries—(134) more than 50%—belonging to the World Trade Organization (WTO)—is below 5%. However, the coronavirus pandemic has pushed the average tariff on COVID-19-specific medical goods to nearly 12%—given the competition for procurement regarding the pandemic. Also, the beggar-thy-neighbor policies (restriction and protectionist measures) are blamed for the sudden tariff increase in coronavirus-related medical products.

To be sure, among the COVID-19 products, some are easier than others when organizations consider their next pivot. For example, medical supplies and personal protective equipment are the low-hanging fruits—in both time and resources required—for firms wanting to pivot in this direction. The medicines category may need more time, resources, and expertise to enter the industry than other categories. We believe this is a promising opportunity that organizations should never miss – given the waning demand in their sector. Above all, hope is not a strategy in this age of the coronavirus. Our COVID-19 resources provide unmatched guides for thriving rather than surviving the disruptions.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.