Japanese Startup Valuation: SMEs'(Startups) Survival Rates and Risk Management

Valuing a company is challenging because several rapidly changing factors must be considered, including industry, cash flow, the firm’s risk profile, and comparable companies, whether based on past transactions or other financial metrics at the time of valuation.

In other words, valuation is both an art and a science, driven by experience and human judgment. That’s one reason it is very rare for two analysts to value a firm and arrive at the same conclusion about their estimates, given the many valuation models and frameworks available to practitioners.

As a result, valuation practitioners often average the results of different models to determine a firm’s final value. For example, they might combine the outcomes of a discounted cash flow (DCF) model with a comparable approach or recent transactions guidance, since each has its own strengths and weaknesses, given assumptions that, in many cases, diverge from the firm’s actual situation.

Why do we Believe Japanese Startups Warrant a Higher Valuation Than it is Currently Acknowledged?

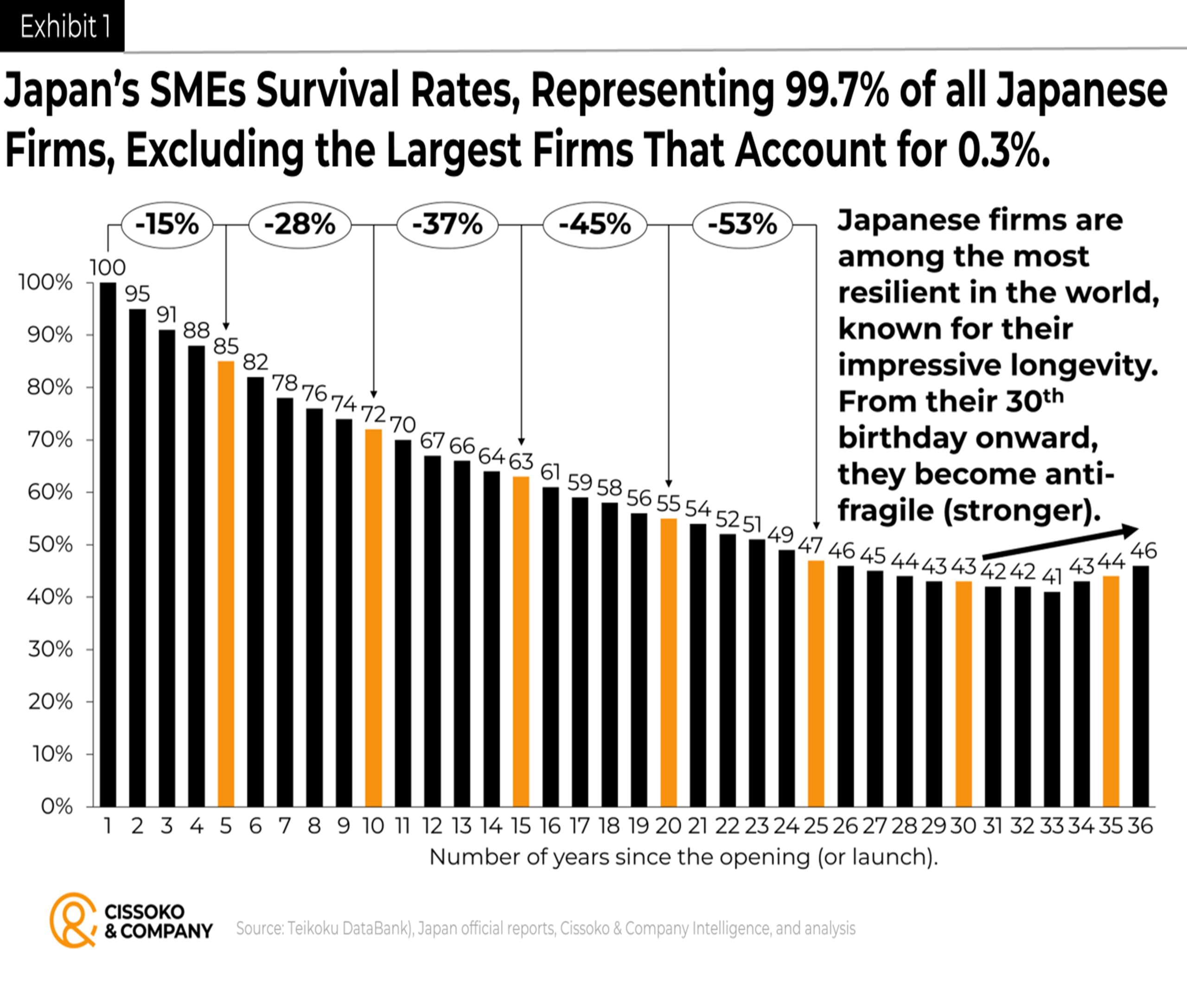

Startups, given their high risk and low survival rates observed worldwide, introduce additional complexity and ambiguity to the art and science of valuation. As such, many analysts and practitioners multiply the survival probability by the future expected cash flow. In other words, the traditional discounted cash flow (DCF) model is adapted to the startup’s risk profile by converting it into an adjusted discounted cash flow (ADCF) model to estimate the startup’s value.

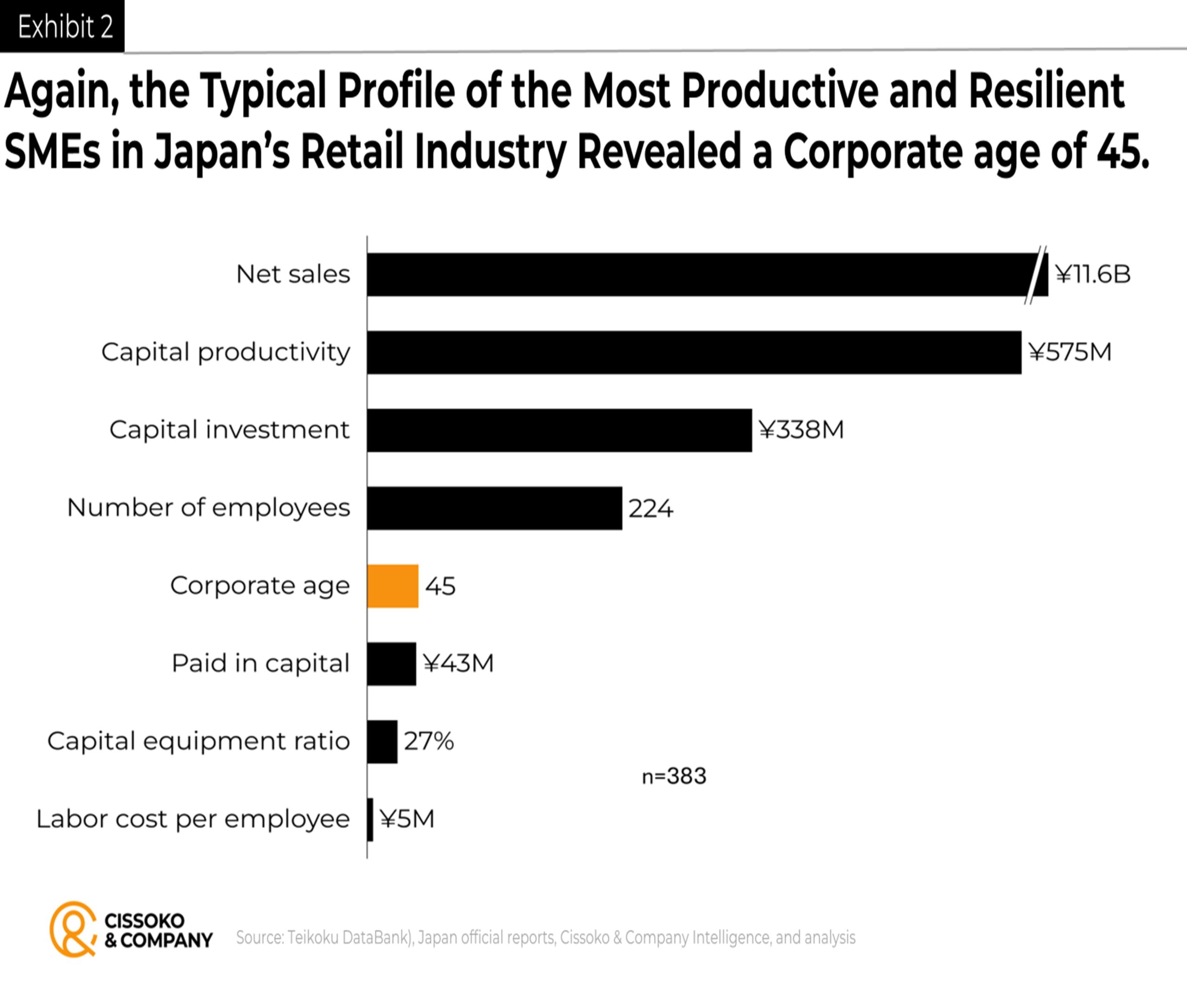

Therefore, higher startup survival rates logically lead to higher startup valuations than those of similar startups in countries or industries with lower survival rates. However, Japanese SMEs, including startups, have higher survival rates than in many other countries, yet still exhibit lower valuations, which is somewhat puzzling.

Therefore, we suspect that many of these newly VC-backed startups may be victims of the flaws inherent in the comparable approach or recent transactions. That is, the methods rely heavily on metrics such as enterprise value-to-sales, price-to-sales, and price-to-book ratios, among others, which can introduce more biases and flaws into the valuation process.

Given that many startups were previously undervalued, the next generation will likely be as well. Similarly, if the wrong comparables were used for prior startups to determine past valuations, the next generation of startups will have their valuations lowered. In other words, each new generation of startups becomes a victim of past valuation biases and flaws, regardless of how their business fundamentals and models differ. For one thing, identifying a ‘perfect’ comparable firm for a valuation purpose is elusive.

Japanese Founders’ Average age and Potential for High Growth

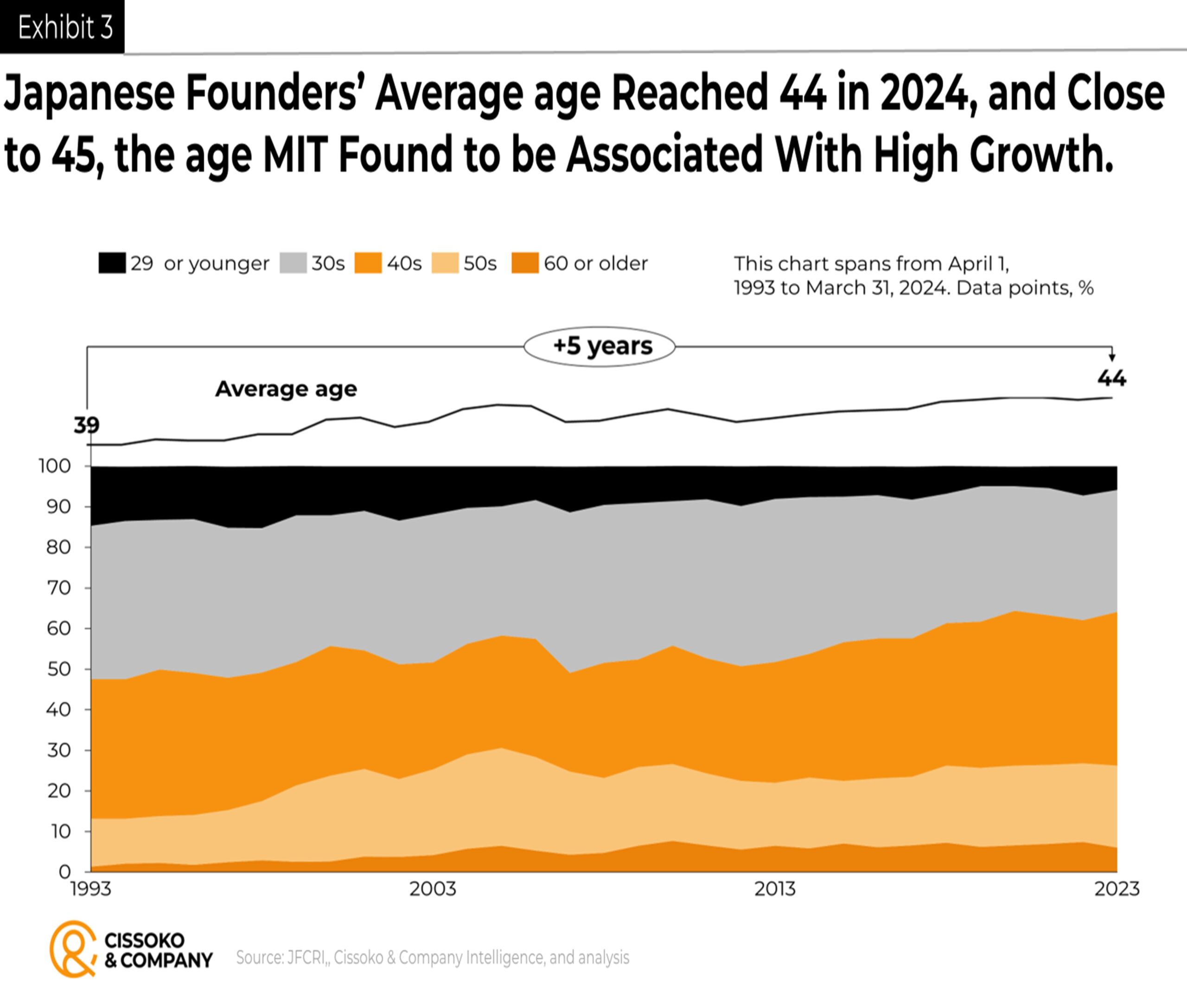

Japan’s average startup founder age hit a milestone on March 31, 2024, marking a notable achievement for entrepreneurship. In fact, a 2019 study from MIT Sloan (before the rise of GenAI) showed that the average age of founders in the top 0.1% of high-growth businesses (in the tech sector, backed by VC(s), and holding a patent) in the US is about 45. A 50-year-old founder is 1.8 times as likely to achieve upper-tail growth as a 30-year-old, according to the analysis.

One reason is that older entrepreneurs often have more management experience, more profound industry knowledge, greater access to financial resources, and stronger social networks.

While the stereotype of the young, tech-savvy founder persists, it’s essential to recognize that young founders can still succeed, as youth often brings sharper cognitive skills, fewer family distractions, and a stronger affinity for technology. Bill Gates and Steve Jobs are prime examples. However, recent studies show that the chance of achieving high-growth success increases with age and experience. The good news is that in practice, many things can be tested with ample data and evidence.

All else being equal, with the average age of Japan’s startup founders reaching 45 and soon surpassing that, we should expect many high-growth companies to emerge from the Land of the Rising Sun if players get solid VC backing and have patents under their belts, as a recent MIT study based on US firms suggests.

Managing Risk and Building Resilience Must be a top Priority for Startups in Times of Artificial Valuation Bubble

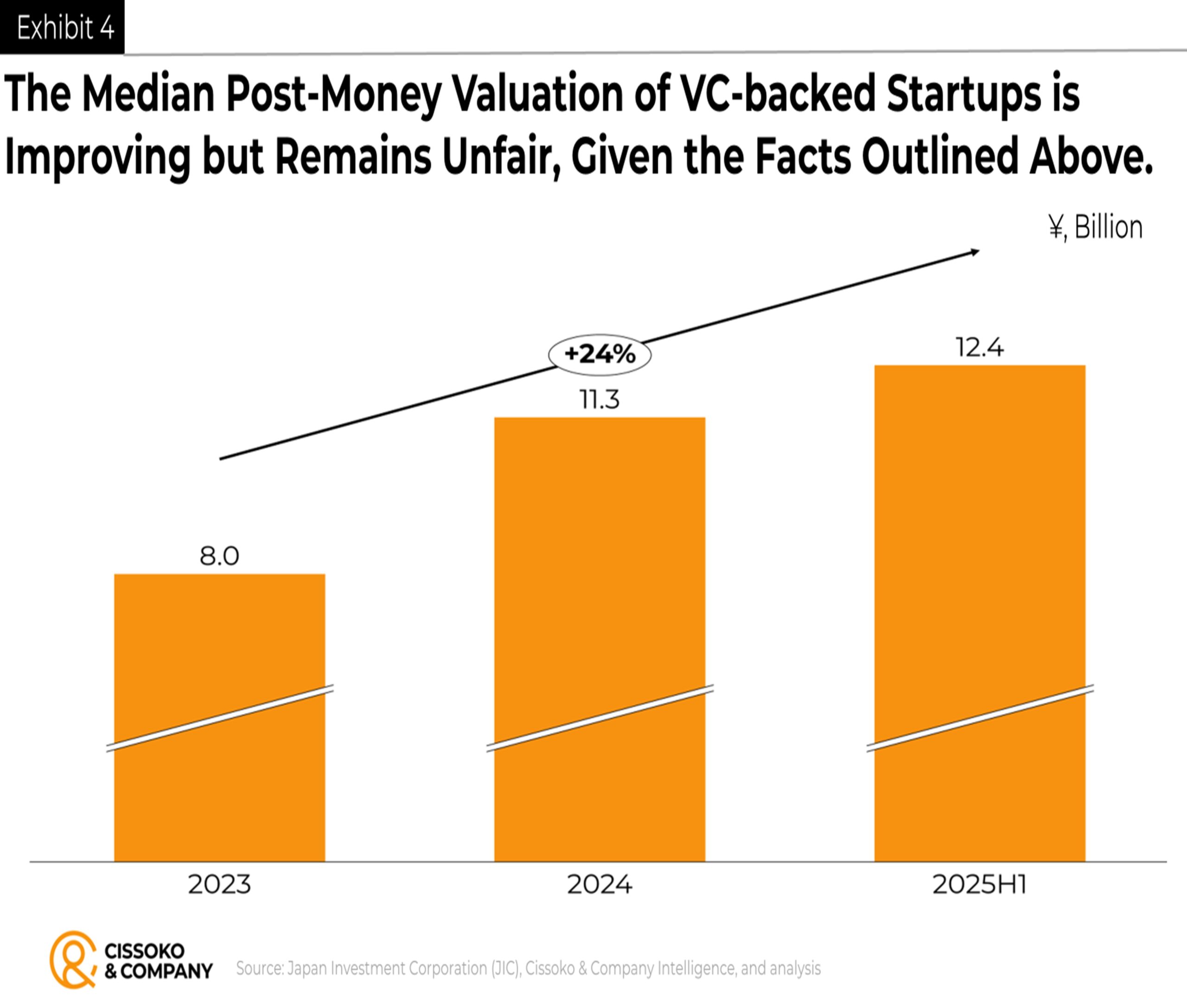

As enthusiasm and anticipation for artificial intelligence continue to grow, the market capitalization of AI-related companies has increased in recent quarters. Moreover, valuations of VC-backed startups continue to skyrocket at an alarming rate.

Consider this: As of January 7, 2025, there were 690 so-called unicorns (startups valued at $1 billion) in the United States, with a combined value of $2.5 trillion. In China, there were 162 unicorns with a combined value of $702 billion, and in the European Union, 107 unicorns with a combined value of $333 billion, according to recent estimates.

To accommodate anticipated demand from AI users, including enterprises and hyperscalers (large technology firms and platforms), hundreds of billions of dollars are being allocated to AI infrastructure development to meet projected AI computing requirements. Consequently, stakeholders across the artificial intelligence ecosystem, both large and small but resourceful ones, have committed hundreds of billions of dollars to develop such infrastructure. Because not all participants possess the substantial financial resources required to meet these obligations, many have resorted to vendor financing, also known as trade credit.

This practice involves a vendor extending credit or providing a loan directly to a buyer, facilitating the purchase of the vendor’s products or services. As a result, the buyer can remit payment over an extended period rather than making an immediate payment.

The issue with such agreements is that they can artificially inflate demand for the parties’ products and services. This occurs because the same funds circulate among these entities, potentially inflating market capitalization through accounting practices reminiscent of those during the dot-com bubble.

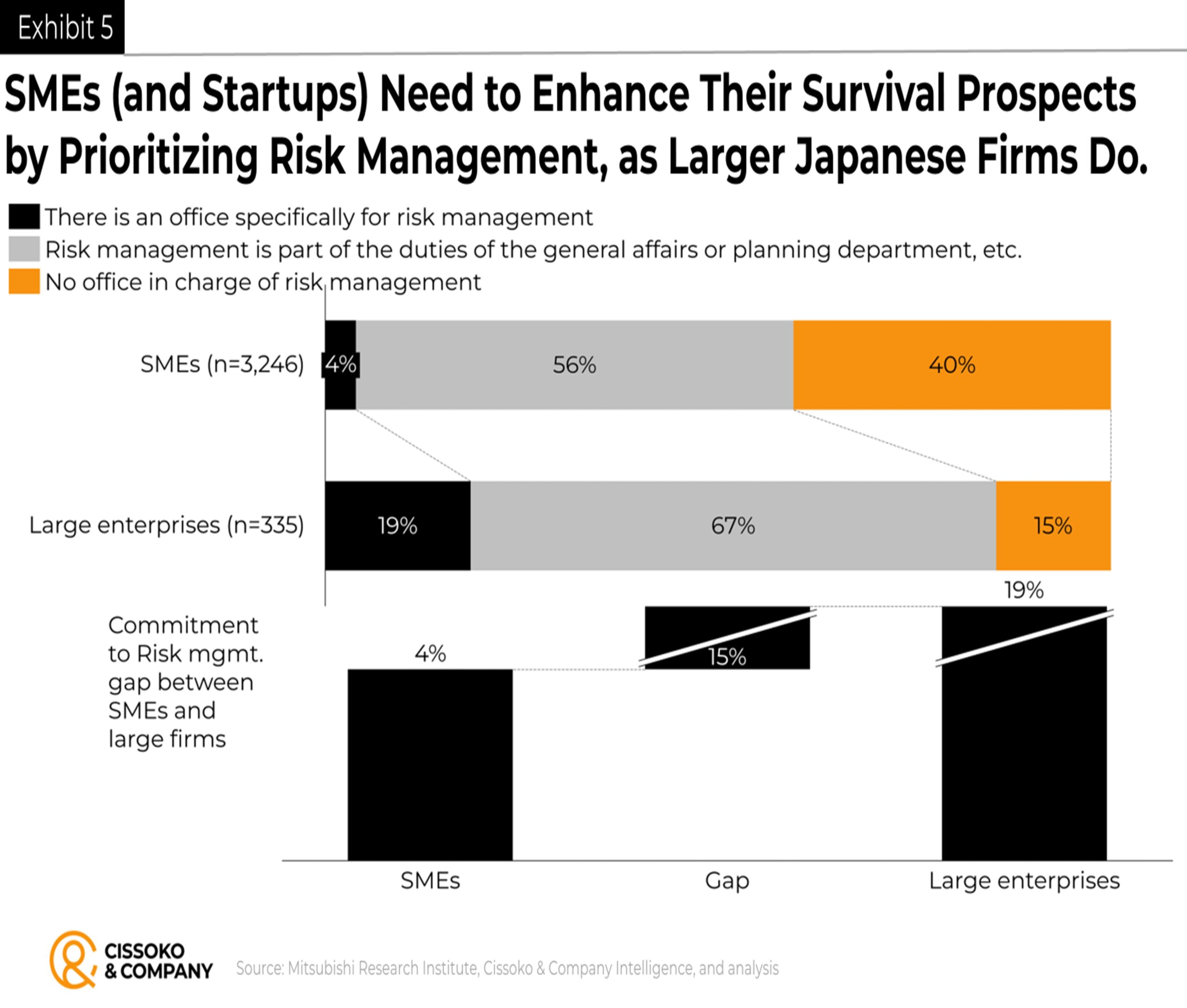

Therefore, to avoid being unprepared for impending financial market disruptions resulting from the deflation of the artificial intelligence bubble, entrepreneurs and small and medium-sized enterprises must intensify their focus on risk management and prioritize it before it is too late.

Get in Touch

We will respond to your message as soon as possible.

Insights to Win

Subscribe to our newsletter for in-depth analysis, reports, and our perspectives on business and economic issues related to the Japanese market and the global economy.